Despite its potential, the battery supply chain faces numerous challenges globally and in India. India, for instance, grapples with limited domestic reserves of critical battery materials, high import costs, and the need for specialized infrastructure, which collectively drive up production costs. Additionally, logistical hurdles, compliance with environmental regulations, and inefficiencies in catering to diverse end-user demands complicate distribution. These challenges underscore the need for robust strategies to ensure a sustainable and efficient battery ecosystem. Australia plays a critical role in the global battery supply chain, holding 25% of lithium, 20% of nickel, and 41% of lead reserves. China has the second-largest lead reserves, accounting for 20%. Meanwhile, Chile leads in lithium reserves at 41%, while Indonesia and Australia share comparable nickel reserves at 22% each.

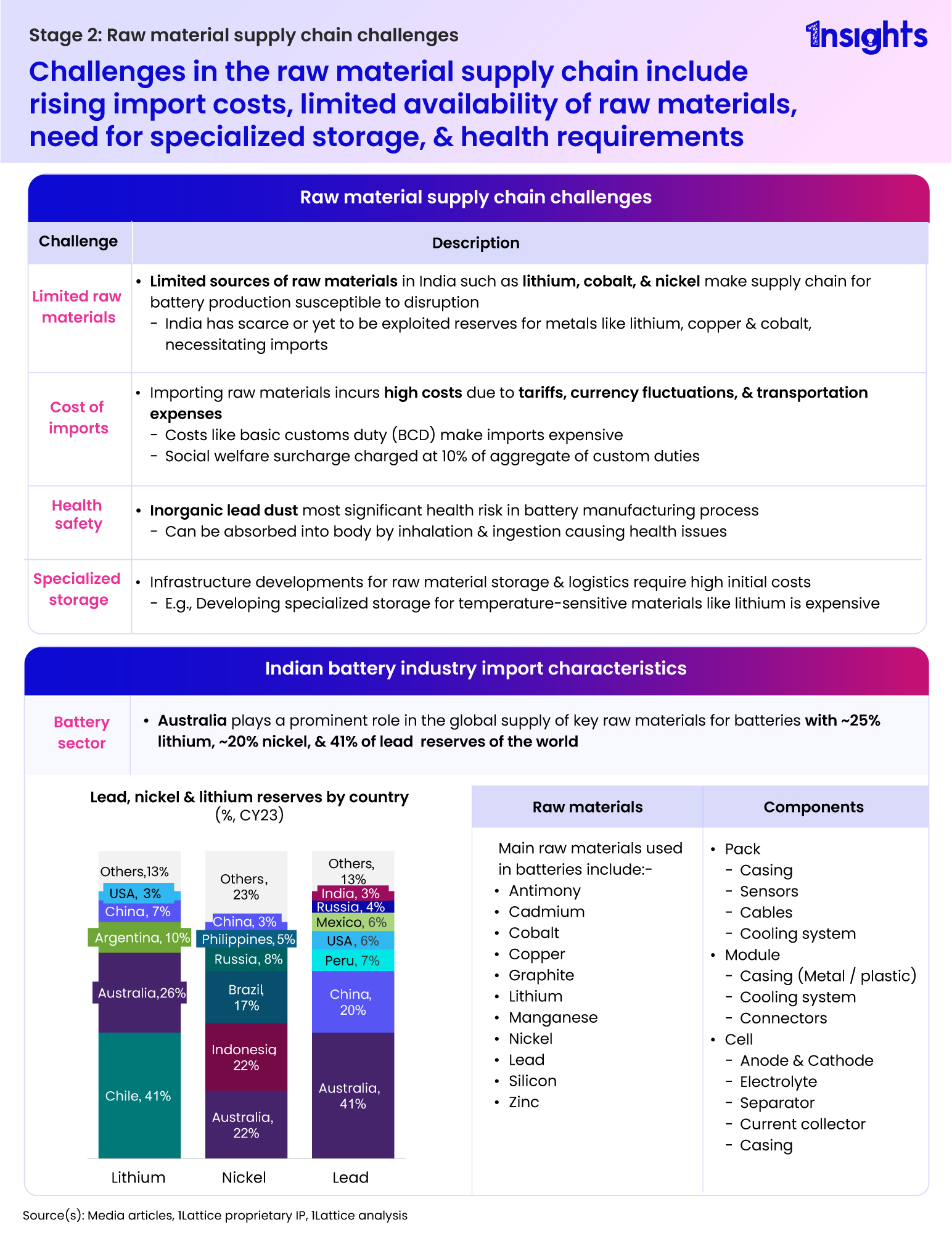

Australia plays a critical role in the global battery supply chain, holding 25% of lithium, 20% of nickel, and 41% of lead reserves. China has the second-largest lead reserves, accounting for 20%. Meanwhile, Chile leads in lithium reserves at 41%, while Indonesia and Australia share comparable nickel reserves at 22% each.

Raw materials supply chain challenges:

- India faces a significant challenge due to limited domestic reserves of key battery materials like lithium, cobalt, and nickel, making it heavily reliant on imports.

- High import costs, driven by tariffs, currency fluctuations, and transportation expenses, increase the overall cost of battery production in India.

- Developing specialized storage infrastructure for temperature-sensitive materials like lithium requires substantial initial investments.

- Health risks in battery manufacturing are notable, with exposure to inorganic lead dust posing serious hazards through inhalation or ingestion.

Distribution supply chain challenges:

- Distribution of batteries faces significant logistical challenges due to their classification as hazardous materials, requiring compliance with regulations like IATA DG rules.

- Battery distributors encounter inefficiencies in catering to diverse end-user industries, as some are focused on specific segments (e.g., UPS batteries) and struggle to meet the demands of emerging markets like EV batteries.

- Compliance with environmental regulations, including e-waste management rules, increases costs and delays in battery distribution due to the need for specialized handling and recycling processes.

Distribution channels for batteries include direct-to-OEM (B2B), online marketplaces (B2B and B2C), modern trade (B2C), and general trade (B2C), with each channel handling products like lead-acid, lithium-ion, and nickel-metal batteries. Prominent companies in battery distribution include Amara Raja, Exide, Moglix, Amazon, and Croma, operating across various channels to meet the needs of industrial and retail customers.