Indian millennials and GenZ are playing a key role in contributing to India’s consumption-led growth story. The internet boom and the subsequent rise of online services in the areas of shopping, food delivery, travel, etc. have given the younger generation a plethora of choices to spend on indulgences.

Having said that, millennials and GenZ have realized the importance of following a healthy savings regime even as the external scenario remains uncertain and ever-changing. Although the overall inclination and awareness to invest is high, most youngsters, especially from tier 1 and tier 2 cities, still require guidance on various investment avenues to generate inflation-beating returns. Many don't invest because they feel they don't have enough time, knowledge, or access to large capital. A new generation of fintech players focusing on micro-savings and change investing is trying to address this problem.

Micro savings apps monitor a user’s spending. Every time the user spends money on shopping, food, etc. via digital means, the app nudges them to save the differential between the amount spent and the nearest round-off to INR 10, INR 50, or INR 100. When such ‘loose change’ cumulatively reaches INR 100, INR 500, or INR 1,000, the app nudges the user to invest it in a financial asset available on its platform.

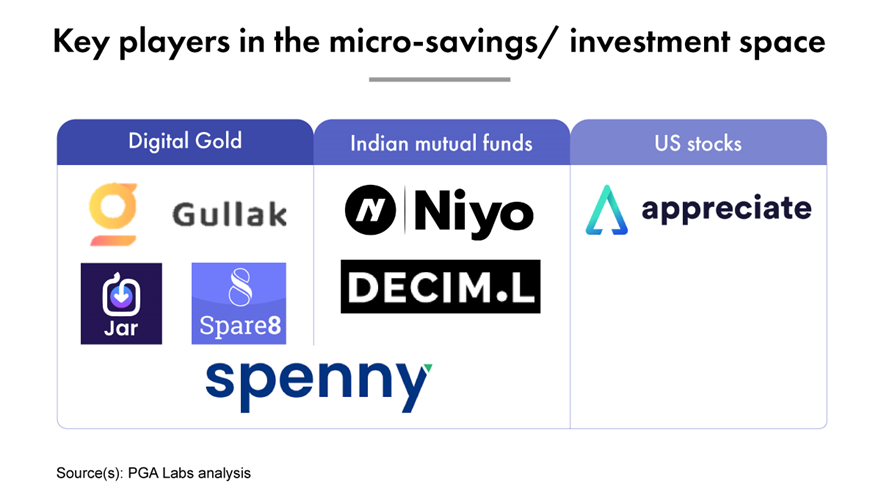

Niyo offers change investing into mutual funds for users who use their app for all banking related services. Apart from Spenny, all the other players are currently focused on a specific investment avenue. Appreciate is the sole player offering change investing into US stocks.

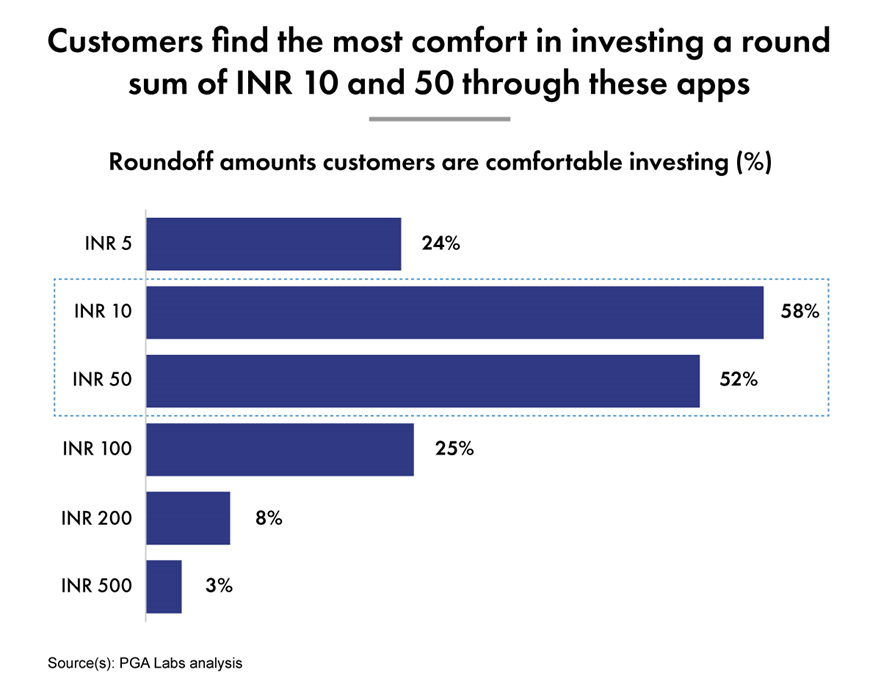

As per a PGA Labs study amongst users of micro-savings apps, more than 50% of respondents prefer saving and investing a round sum of INR 10 or INR 50, depending on the app functionality. It has been observed that 77% of customers falling in the age bracket of 18 – 24 years prefer investing a round sum of INR 10. This can be attributed to the fact that a vast majority of these youngsters are students with very limited or no income source. Additionally, some of them have just started with their jobs and hence are still figuring out their savings habits.

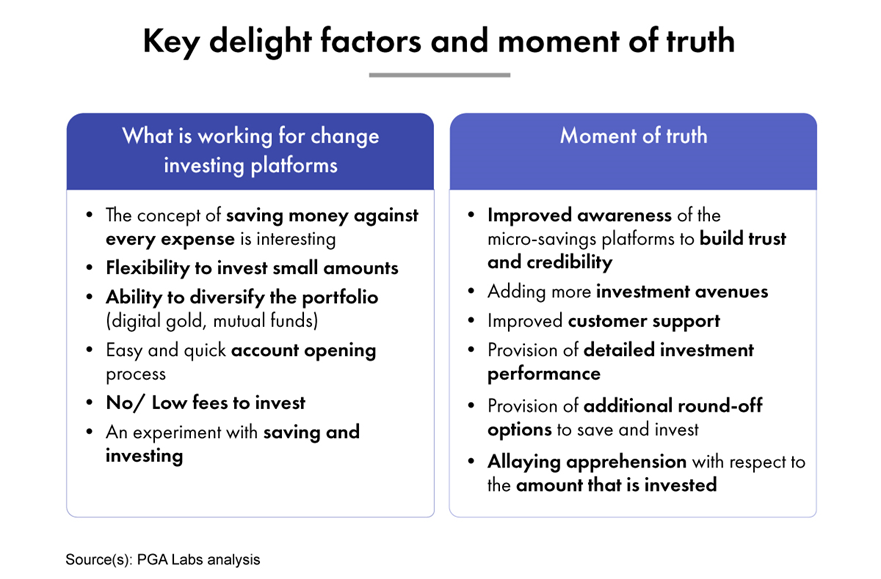

Millennial

and GenZ users are fascinated with the concept of a savings plus investment

product. The process involving micro-savings on each expense and investing the

sum into an asset is helping solve the mindset of not being able to save enough

and invest. Users would like these apps to add more investment products to

access a wider set of assets. Current awareness about these apps is

predominantly through word of mouth and hence formal marketing communication

will help widen the reach and build customer confidence.