Globally, neobanks are ‘digital only’ banks specializing in financial products, like deposits, payments, debit cards, money transfers, lending, and more. They cater to the increasing demand for technology-based banking services from tech-savvy consumers who may find traditional banking procedures tedious and cumbersome. Unlike traditional banks, neobanks primarily operate online and do not have physical branches, allowing them to devote more capital towards improving the customer experience through technology and faster turnaround time.

Although neobanks are relatively new, they are registering impressive growth, with more than 200 neobanks worldwide. In the Indian context, however, neobanks are fintech firms that offer a banking app in partnership with a traditional bank. While the partner bank plays the role of providing the core banking needs, the neobanking app helps provide a seamless delivery of these services and enhanced engagement experience to customers on behalf of the partner bank.

In the following sections, we look at the regulatory landscape surrounding neobanks in India.

The RBI does not recognize neobanking players as banks!

The Government of India has made significant progress in advancing the fintech ecosystem, but neobanks are not currently recognized as banks by the Reserve Bank of India (RBI). In November 2021, the RBI indicated that it plans to regulate the establishment of digital banks and neobanks. It has reiterated its position that traditional banks partnering with neobanks should not allow the neobanks to refer to themselves as "banks," and should also impose strict outsourcing obligations. These obligations may include requirements for continuous monitoring, data security, grievance handling, and regular audits, as well as giving the RBI access to the accounts and transaction records of neobanks.

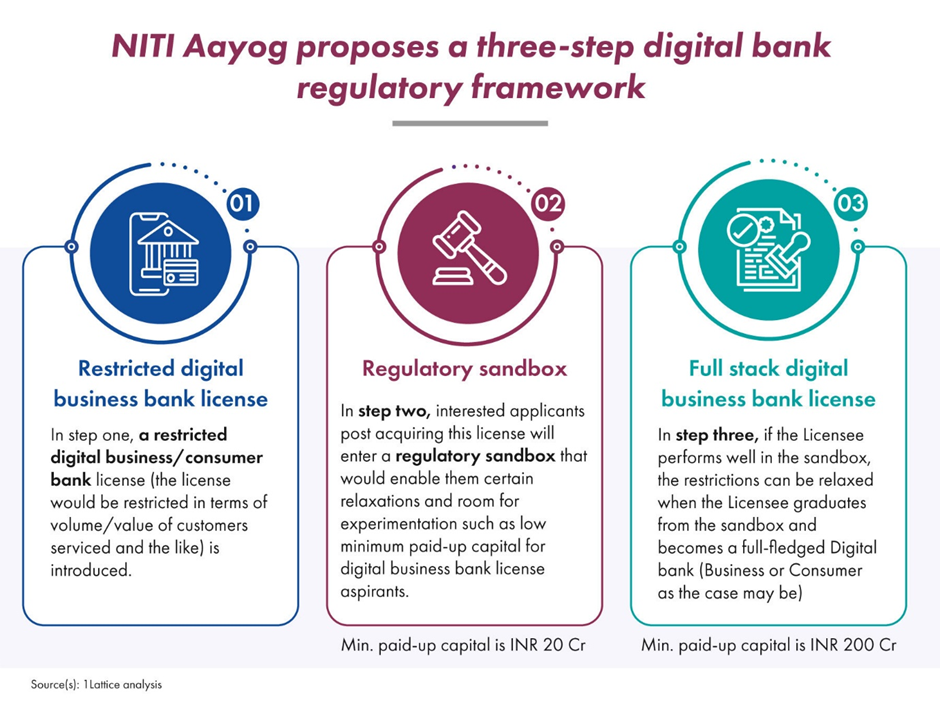

NITI Aayog’s views on digital banks

The NITI Aayog released a discussion paper called "Digital Banks (A Proposal for Licensing & Regulatory Regime for India)," which suggests the need for a framework to allow neobanks to become fully licensed digital banks. The report recognizes that India has the necessary technology infrastructure to support digital banks and that a regulatory framework is needed to take advantage of this. The NITI Aayog has also highlighted the challenges faced by neobanks, including:

- The obsolescence of the partner bank’s core banking system leading to failure in partnerships that neobanks currently have

- High capital cost - Lack of low-cost deposits and the need to rely on expensive equity capital for innovation and operations reduces profitability for current players in the neobanking market

- No Entry Barrier – The absence of licensing framework may lead to creating opportunities for actors who may not meet the necessary standards, leading to potential risks to consumer protection

- Limited

revenue potential – Neobanks currently earn fee-based revenue wherever they act

as channel partners (account opening and onboarding, investment opportunities,

credit), and potentially earn a percentage of interchange on card payments

In the process of obtaining a license, the RBI and the applicant will agree on a set of metrics to monitor the licensee's progress. These metrics may include the cost of acquiring a customer, the volume and value of credit provided to micro, small, and medium enterprises (MSMEs), the licensee's technological readiness, and compliance with prudential regulations, among other things

A light at the end of the tunnel?

In

the process of obtaining a license, the RBI and the applicant will agree on a

set of metrics to monitor the licensee's progress. These metrics may include

the cost of acquiring a customer, the volume and value of credit provided to micro,

small, and medium enterprises (MSMEs), the licensee's technological readiness,

and compliance with prudential regulations, among other things