In India, around 65% of the population lives in rural areas, where income patterns, distribution channels, and financial needs differ from urban counterparts. Commercial financial institutions focus more on urban areas due to higher awareness, easier distribution, and stable incomes, resulting in greater insurance penetration in cities than in rural regions. India's insurance penetration stood at 3.7% in FY24, still below the global average of 7%. Life insurance, in particular, saw a slight decline to 2.8%, highlighting the need for stronger adoption, especially in rural areas

In today’s newsletter, we explore the life insurance landscape in Tier 3 markets—a segment that presents unique challenges and untapped opportunities. Through in-depth interviews with insurance agents in these regions, we've identified key trends, customer mindsets, and strategies shaping the future of life insurance in emerging markets.

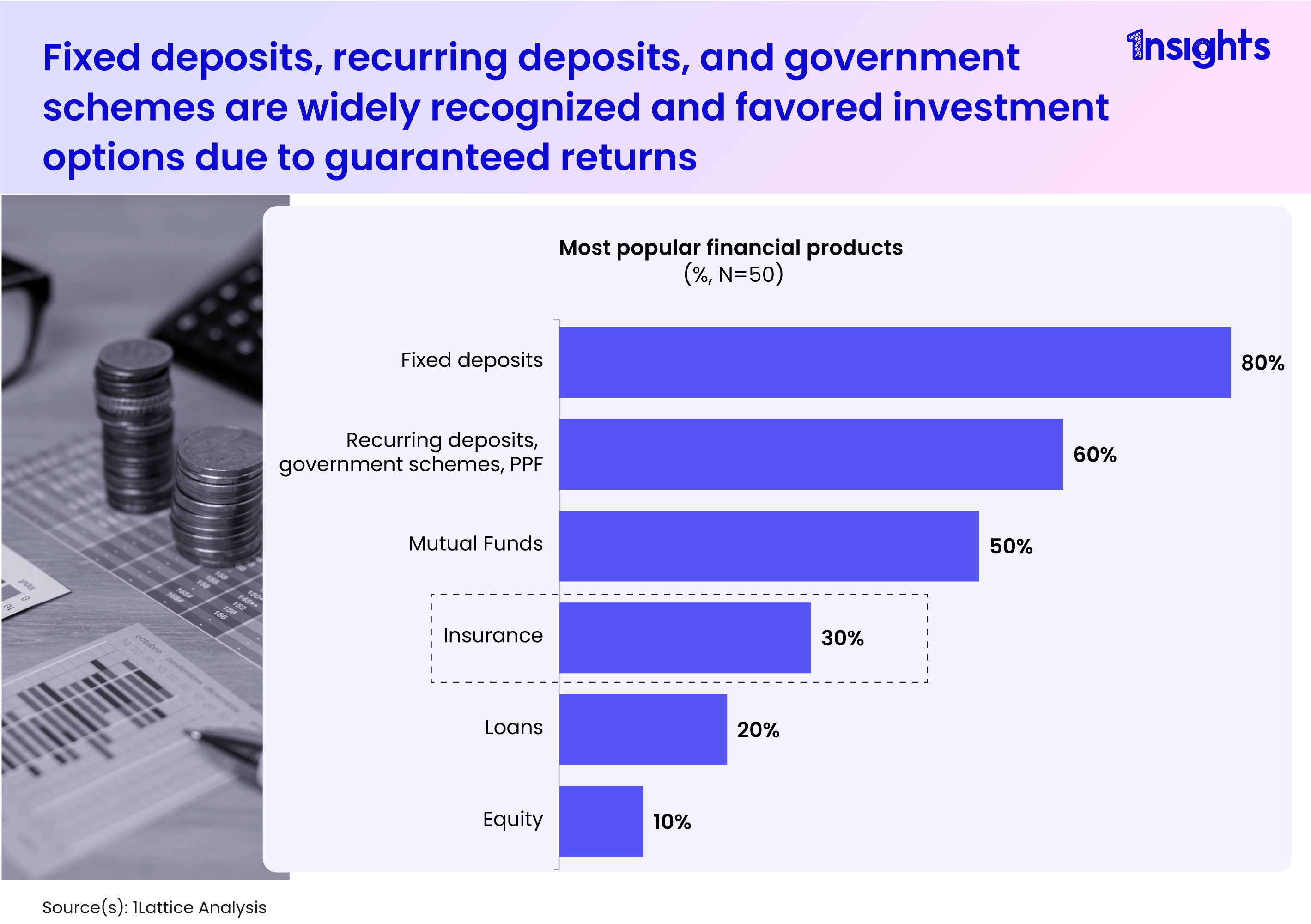

Consumers in Tier 3 markets show a strong preference for fixed deposits, recurring deposits, and government schemes due to their guaranteed returns and lower risk. In contrast, life insurance ranks lower, with only 30% preference, despite its long-term financial security benefits.

Consumers in Tier 3 markets show a strong preference for fixed deposits, recurring deposits, and government schemes due to their guaranteed returns and lower risk. In contrast, life insurance ranks lower, with only 30% preference, despite its long-term financial security benefits.

In urban centers, financial awareness is significantly higher due to TV, outdoor ads, and social media campaigns, whereas rural areas have limited exposure. Fixed deposits, recurring deposits, and government schemes remain the preferred investment choices across demographics due to their assured returns.

However, mutual funds are gaining traction, especially for short-to-medium-term goals like children's education and marriage, driven by their high returns and liquidity. Despite this, stock and equity investments see low adoption due to perceived risks and a lack of financial knowledge, particularly in rural areas

Savings plans are the most preferred option due to their guaranteed returns and tax benefits. However, concerns over low returns and payout structures persist

Term plans, while offering high coverage and affordability, still face challenges as customers hesitate due to long-term commitments and eligibility criteria. Additionally, the preference for tangible returns makes pure protection plans less attractive

Retirement plans, though providing financial security and flexibility, are met with apprehension due to their longer tenure and concerns over tangible returns

ULIPs, in particular, face the highest level of customer concerns, such as market risk, high charges, lock-in periods, and complexity, which make them less appealing despite their wealth accumulation benefits

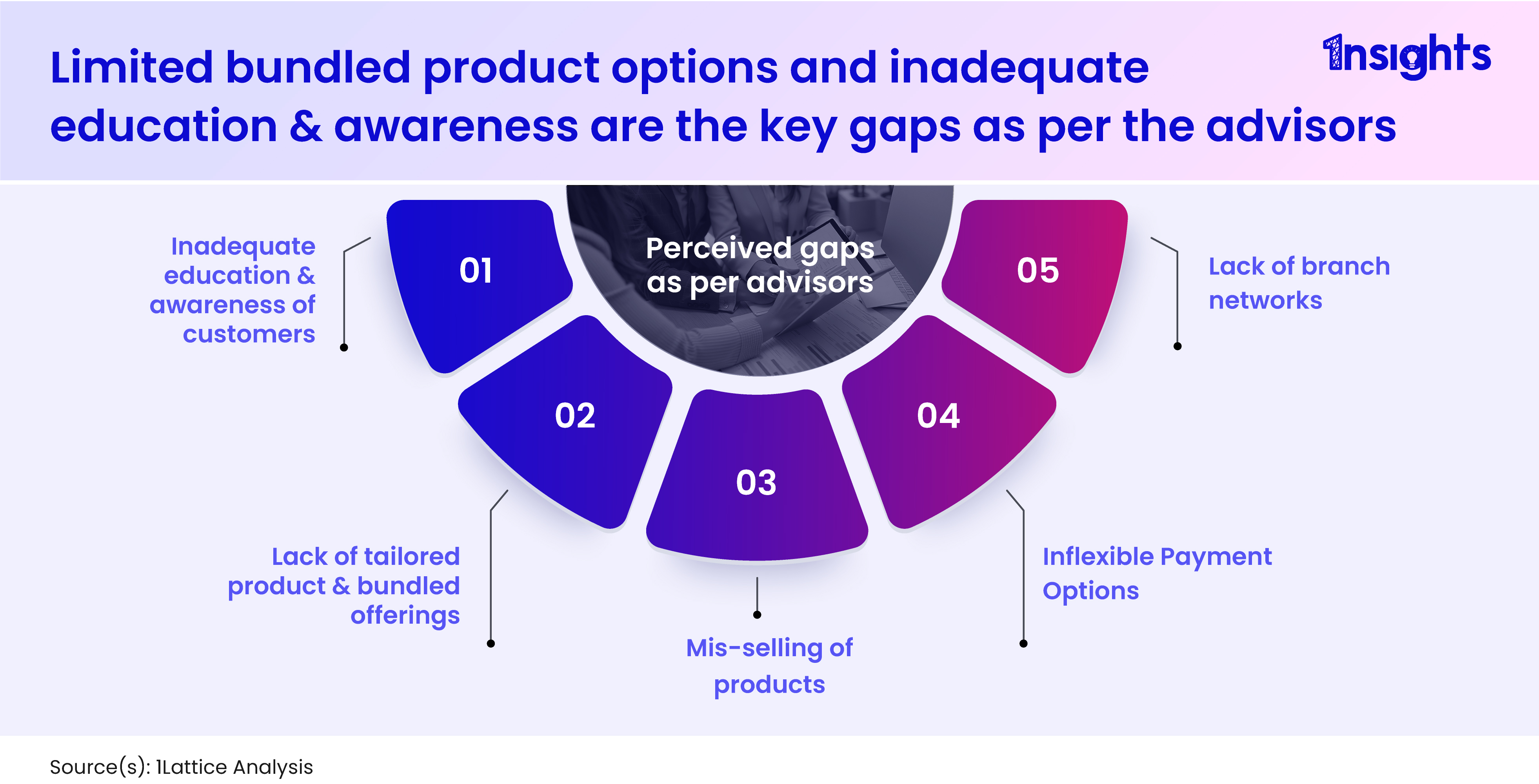

Lack of campaigns on customer education about the importance and benefits of LI, and how it aligns with overall financial planning

Lack of bundled product offerings; combination of health & life insurance. Short-term plans with low premiums. Affordable micro-insurance products

Aggressive targets resulting in mis-selling, damaging the customer’s relationship with the RM, and the life insurer

Flexible premium payment options to match cash flow & preferences, often requesting changes from monthly to quarterly, annually, or vice versa

Expanding branch networks, physical accessibility

Build on customer relationships by offering at-home services, sending birthday or anniversary cards or gifts, to customers completing policy tenure

In conclusion, the Tier 3 life insurance market presents both significant opportunities and pressing challenges. While customer demand for flexible, transparent, and reliable insurance products is rising, gaps in financial literacy, product accessibility, and trust continue to hinder wider adoption.

Advisors play a crucial role in bridging this divide, yet they face obstacles such as mis-selling pressures, rigid product structures, and limited customer education initiatives. Addressing these challenges through strategic outreach, innovative product bundling, and enhanced customer engagement can unlock tremendous growth potential. As the industry evolves, insurers must adapt to the unique needs of these emerging markets to foster deeper financial inclusion.

We assisted a leading private life insurer in understanding customer perceptions of life insurance, including awareness, demographics, brand value, and the challenges faced by agents in the sales and marketing process. If you're a life insurer or BFSI player looking for similar insights, let's connect!