The housing finance sector in India is witnessing an upward trajectory due to government initiatives for affordable housing (interest subsidies under Pradhan Mantri Awas Yojana), the nuclearization of families, and the demand for housing in non-metro cities. Increasing urbanization and low mortgage rates are the two main elements driving market expansion, particularly among the younger generation.

During the period 2022-27, the Indian housing finance industry is expected to increase at a compounded annual growth rate (CAGR) of ~21%. Although banks have traditionally been the major contributors; Housing Finance Companies (HFCs) are steadily improving their market share thanks to flexible lending products and competitive interest rates.

In

the following sections, we try to understand how HFCs stack up against a bank

from the eye of the customer A

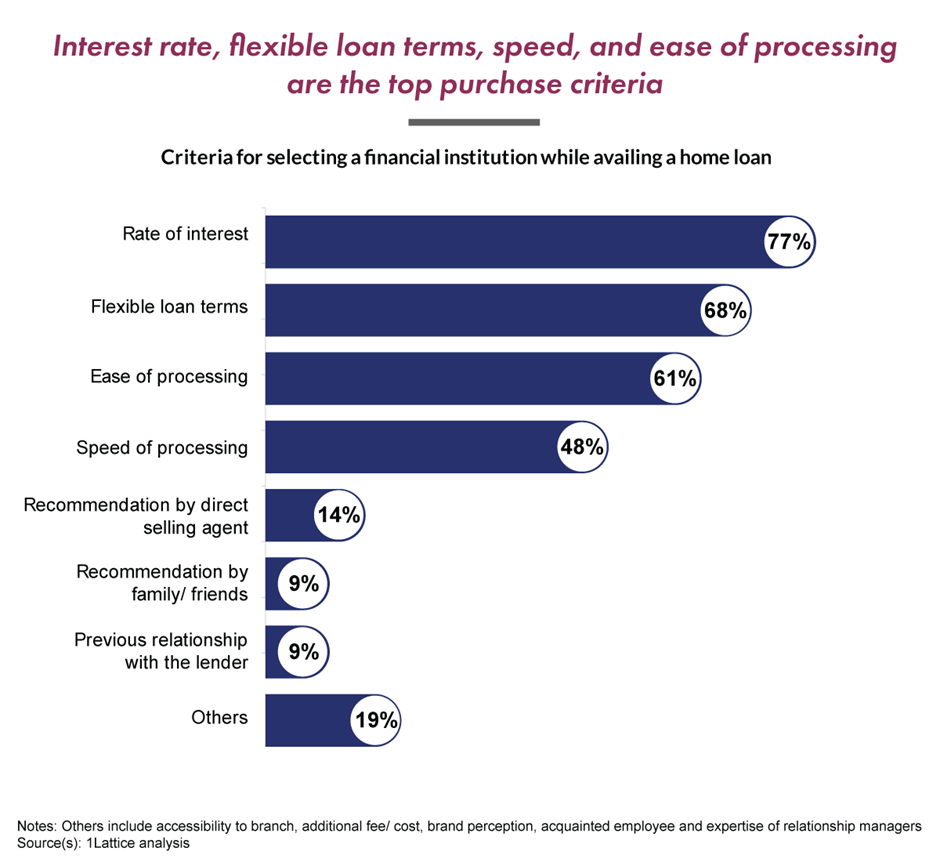

home loan being a significant long-term financial commitment, the rate of

interest is the biggest decision-making trigger when a customer has to choose

between different banks and HFCs. Apart from the interest rate, our research

indicates that flexible loan terms and processing ease & speed are most

critical. HFCs usually score better on processing time since their eligibility

criteria are not as stringent as that of a bank

A

home loan being a significant long-term financial commitment, the rate of

interest is the biggest decision-making trigger when a customer has to choose

between different banks and HFCs. Apart from the interest rate, our research

indicates that flexible loan terms and processing ease & speed are most

critical. HFCs usually score better on processing time since their eligibility

criteria are not as stringent as that of a bank

Customers tend to prefer HFCs over a bank as they provide.

- Flexibility with regard to providing higher loan quantum - In comparison to banks, HFCs are more suitable for many consumers seeking a larger loan amount. When calculating the market value of a property, banks typically exclude stamp duty and registration fees. HFCs, on the other hand, are more flexible in including these in the overall cost of the property

- Less stringent while assessing creditworthiness - Banks have stringent regulations when it comes to approving a home loan. This is also true for credit scores. Banks only provide housing loans to people with perfect credit scores, whereas HFCs are more flexible and will consider applications with low credit scores

A

customer with a good credit score would usually get a relatively cheaper loan

from a bank as compared to an HFC.

A

customer with a good credit score would usually get a relatively cheaper loan

from a bank as compared to an HFC.

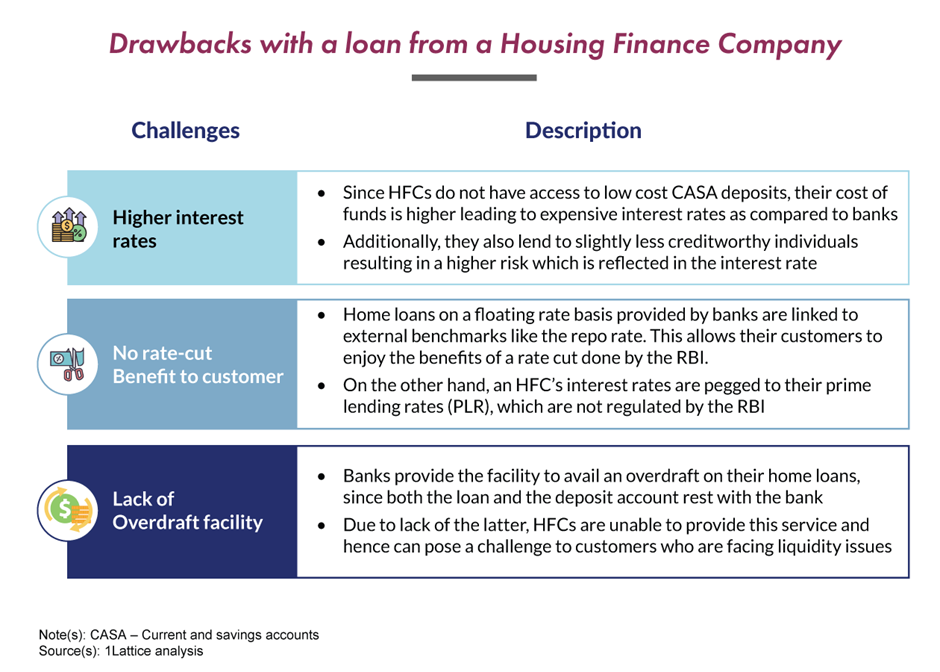

Unlike

a bank, HFCs may choose not to pass on RBI’s rate cut benefits to their

customers since their rates are not linked to the repo rate. They, however, do

pass on slight benefits in order to stay competitive and avoid customer churn.

HFCs do not offer an overdraft facility against the loan which can be a

deterrent if a customer has liquidity issues.

With

the average age of home buyers coming down, there has also been a natural shift

in the way people buy homes & more importantly, the way people approach

housing finance. A thriving market for HFCs is critical for the economy,

considering banks try to restrict their home loan disbursals to prime

borrowers. The merger between HDFC (the largest HFC by loan book) and HDFC bank

is set to have a major impact on the market. We at 1Lattice foresee the

following challenges in the mid-term:

- Potential reduction in the market share of HFCs and a simultaneous increase in that of banks

- Impact on growth and margins of HFCs due to increased competition to low-cost borrowing of banks

- HFCs

may be driven towards riskier developer loans, which come with asset quality

risks