Behind every fertility journey, prenatal screening, and high-risk pregnancy assessment lies a technology that has become indispensable to modern healthcare.

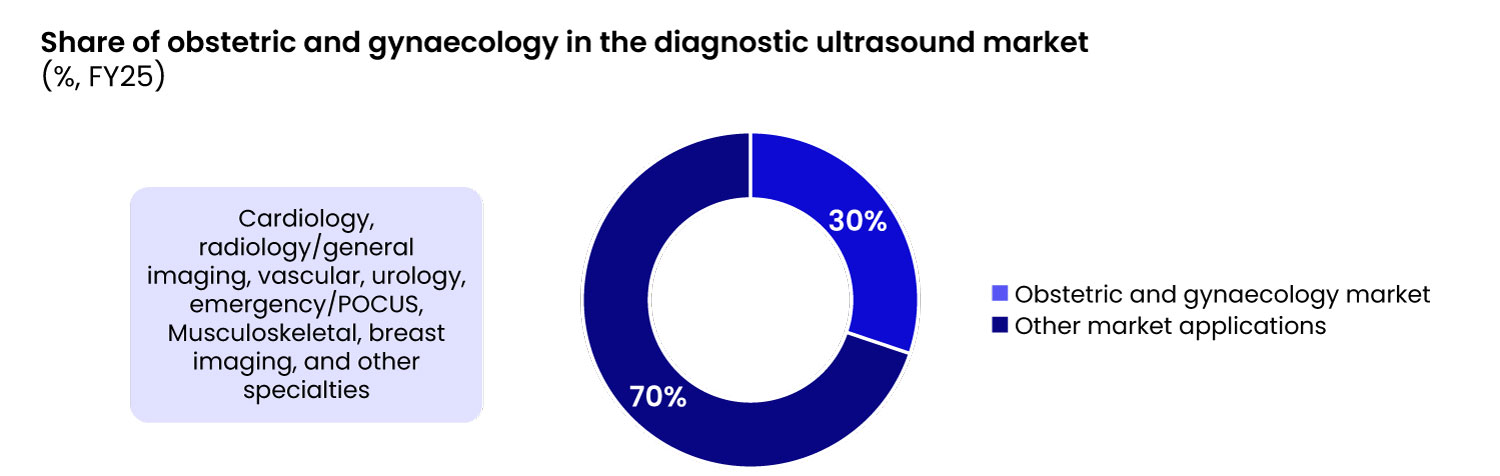

This edition of the newsletter highlights the growing importance of obstetric and gynaecology (OB/GYN) ultrasound, a cornerstone of women’s healthcare that accounts for nearly 30% of the diagnostic ultrasound market. Unlike many imaging applications that are episodic, OB/GYN ultrasound supports the entire maternal and reproductive care continuum, from fertility assessment and early pregnancy confirmation to fetal anomaly screening, high-risk pregnancy monitoring, delivery planning, and postpartum evaluation.

Driven by India’s high annual birth volumes and increasing emphasis on preventive screening and fertility care, OB/GYN ultrasound continues to witness sustained demand across hospitals and diagnostic centers. Its expanding role in clinical decision-making and personalized patient management underscores its significance as one of the most critical and frequently utilized imaging modalities in modern healthcare.

High OB/GYN Ultrasound Demand

-

India accounts for nearly one-fifth of global births, with ~23–25Mn births annually, making obstetric ultrasound one of the country's highest-volume imaging procedures. Multiple ultrasound examinations are routinely performed throughout pregnancy, driving sustained demand for OB/GYN ultrasound systems across hospitals and diagnostic centers

-

In India, these services are heavily regulated by the PC&PNDT Act, 1994, to prevent sex-selection, with specialized scans routinely performed by qualified gynaecologists and radiologists

-

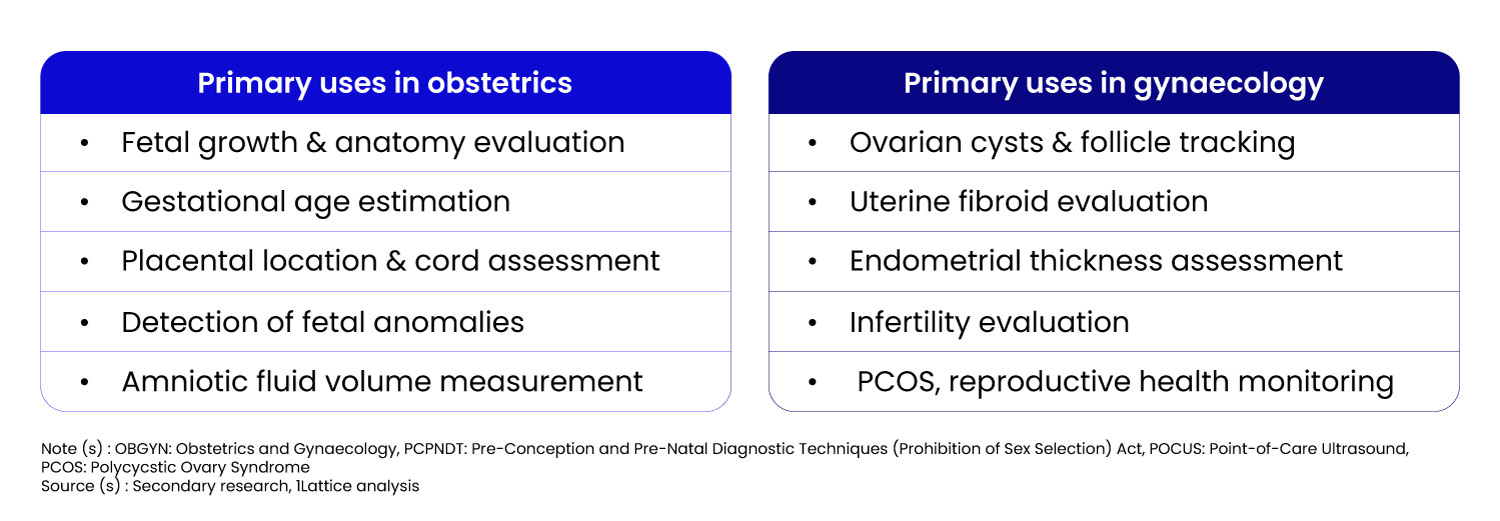

Unlike many other applications that are episodic, OB/GYN ultrasound is used repeatedly across the maternal patient journey: from pre-conception fertility assessment and early pregnancy confirmation to anomaly screening, high-risk monitoring, delivery planning, and postpartum evaluation

-

Its expanding role in preventive screening, risk stratification, and fertility care continues to drive steady growth across both public and private healthcare settings

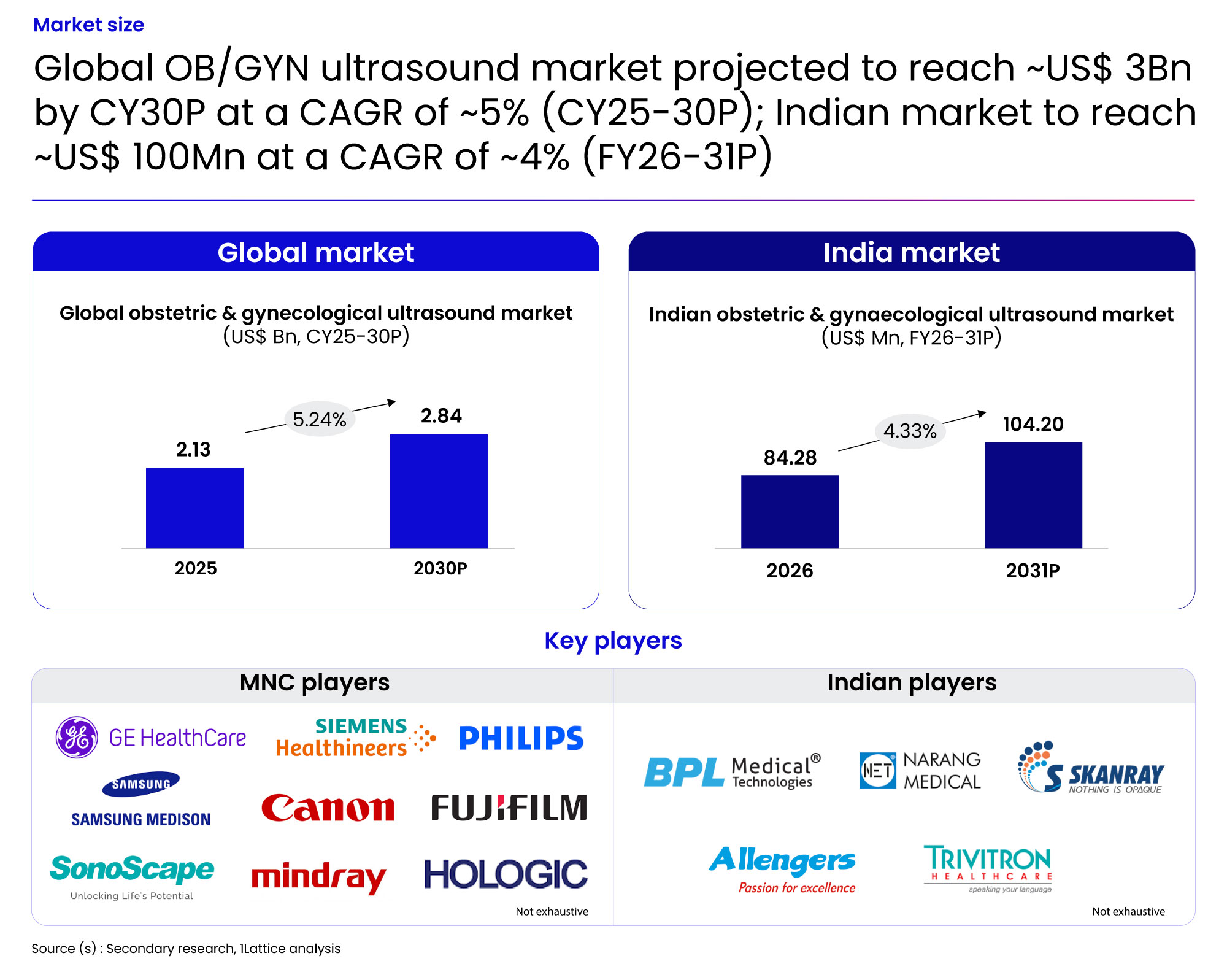

Building on the clinical importance of OB/GYN ultrasound, the market continues to demonstrate steady growth driven by increasing imaging demand, technological advancements, and expanding access to maternal healthcare services. The global obstetric and gynaecological ultrasound market is projected to grow from US$ 2.13Bn in 2025 to US$ 2.84Bn by CY30P, while the Indian market is expected to expand from US$ 84.3Mn in FY26 to US$ 104.2Mn by FY31, reflecting sustained adoption across both developed and emerging healthcare systems.

The competitive landscape remains led by established multinational players, including GE HealthCare, Philips, Siemens Healthineers, Canon, Samsung Medison, Fujifilm, Mindray, SonoScape, and Hologic, alongside a growing presence of domestic manufacturers such as BPL Medical Technologies, Trivitron Healthcare, Allengers, Narang Medical, and Skanray, highlighting increasing local capabilities and market participation.

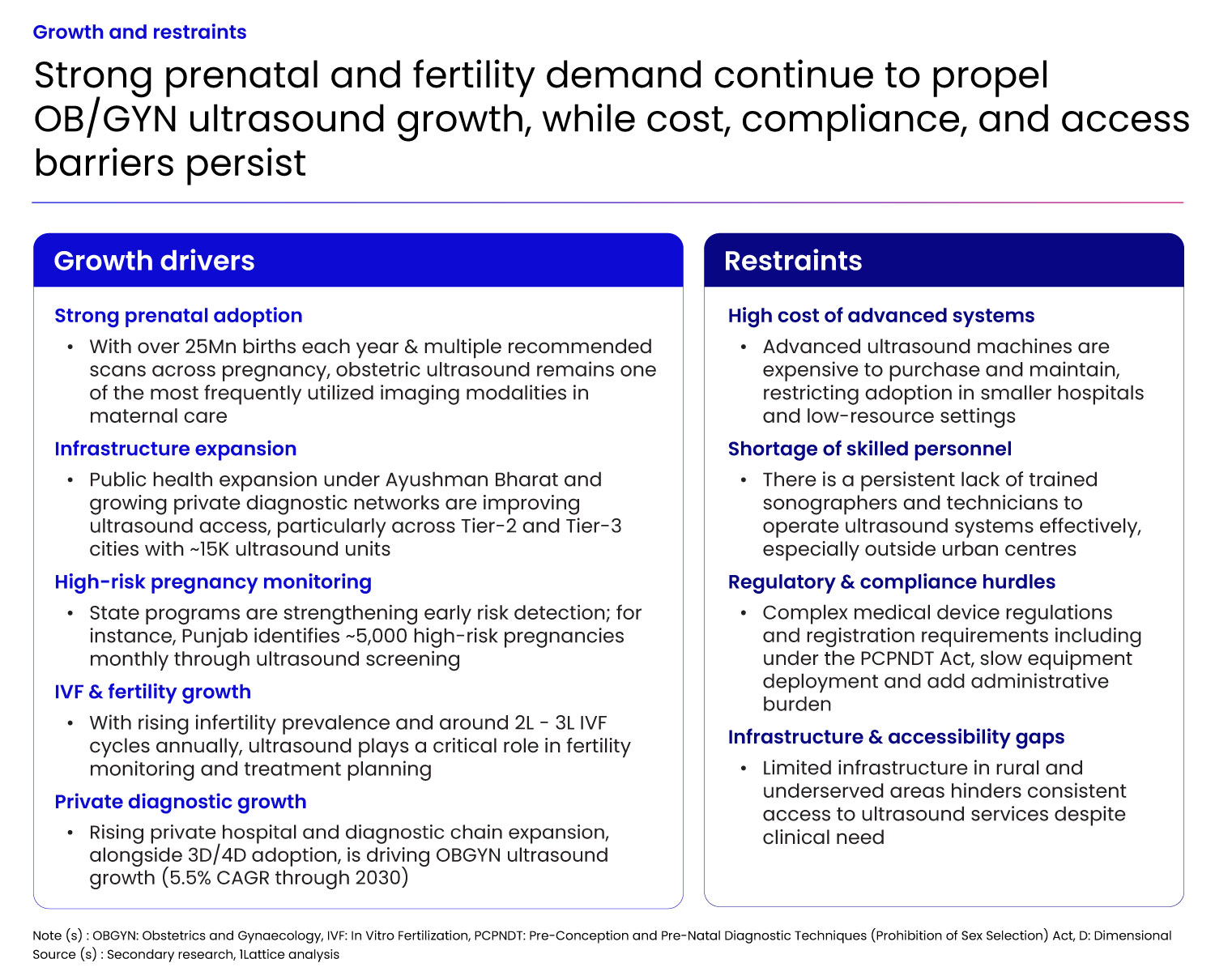

Despite a mature and steadily expanding market outlook, the growth trajectory of OB/GYN ultrasound continues to be influenced by a dynamic mix of favorable demand fundamentals and structural constraints. Sustained prenatal imaging requirements driven by India’s high birth volumes, expanding public healthcare initiatives, strengthening early-risk detection programs, and rising infertility rates are reinforcing the indispensable role of ultrasound across the maternal and reproductive care continuum. Furthermore, increasing investments by private hospitals and diagnostic chains, alongside the growing adoption of advanced 3D/4D imaging technologies, are expected to support continued market expansion in the coming years.

At the same time, several challenges continue to temper the pace of adoption. The significant upfront investment and maintenance costs associated with premium ultrasound systems limit accessibility for smaller healthcare providers, while a shortage of trained sonographers and technicians affects efficient utilization, particularly outside major urban centers. In addition, stringent regulatory requirements under the PCPNDT Act and persistent infrastructure gaps in rural and underserved regions create operational complexities and restrict equitable access to diagnostic services. Overcoming these barriers through targeted investments in affordability, workforce development, and healthcare infrastructure will be essential to unlocking the next phase of growth for the OB/GYN ultrasound market.

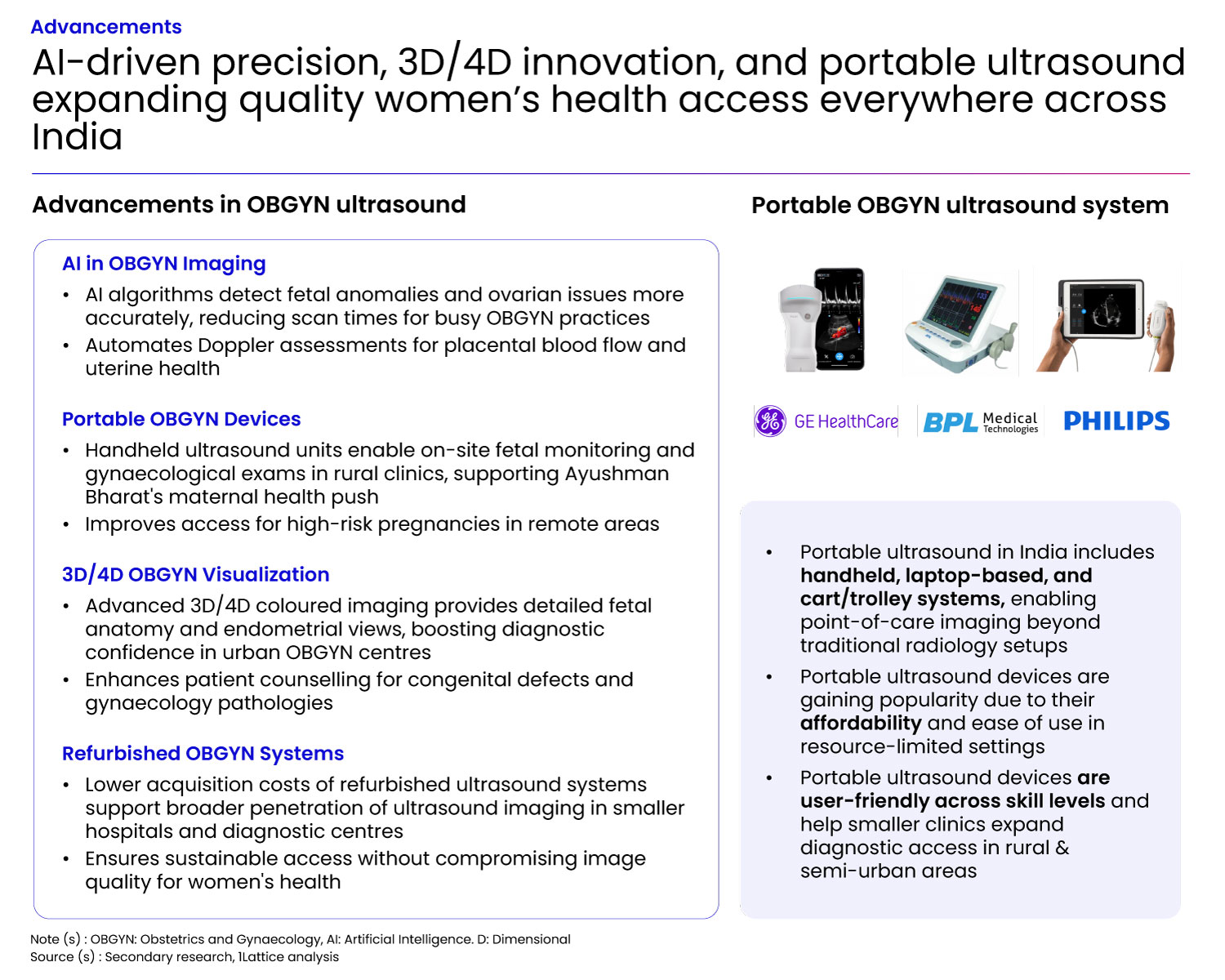

The OB/GYN ultrasound landscape is undergoing a rapid technological transformation, with innovations in artificial intelligence, advanced imaging, and portable platforms redefining the delivery of women’s healthcare. AI-powered algorithms are enhancing diagnostic precision by enabling faster and more accurate detection of fetal anomalies and gynecological conditions, while automating complex assessments to improve workflow efficiency. At the same time, high-resolution 3D/4D visualization is providing clinicians with richer anatomical insights, strengthening prenatal diagnostics, patient counselling, and clinical confidence.

A parallel shift toward portability and affordability is expanding access to ultrasound services beyond conventional hospital settings. Handheld, laptop-based, and cart-mounted systems are enabling point-of-care imaging in rural clinics, community health centres, and remote locations, supporting broader maternal health initiatives and improving access for high-risk pregnancies. Additionally, the increasing adoption of refurbished ultrasound systems is lowering acquisition costs for smaller healthcare providers without compromising diagnostic quality, making advanced imaging more accessible across India’s evolving healthcare ecosystem.