This edition of the newsletter highlights the evolving cardiovascular intervention landscape in India, driven by a high and growing burden of cardiovascular diseases (CVD), increasing procedural volumes, and expanding access to interventional care. The sector is witnessing significant momentum led by rising adoption of minimally invasive procedures, expansion of cath lab infrastructure, and growing focus on advanced structural heart interventions. This report presents a concise overview of India’s cardiac intervention market, covering disease burden, procedure trends, key drivers and challenges, and emerging opportunities.

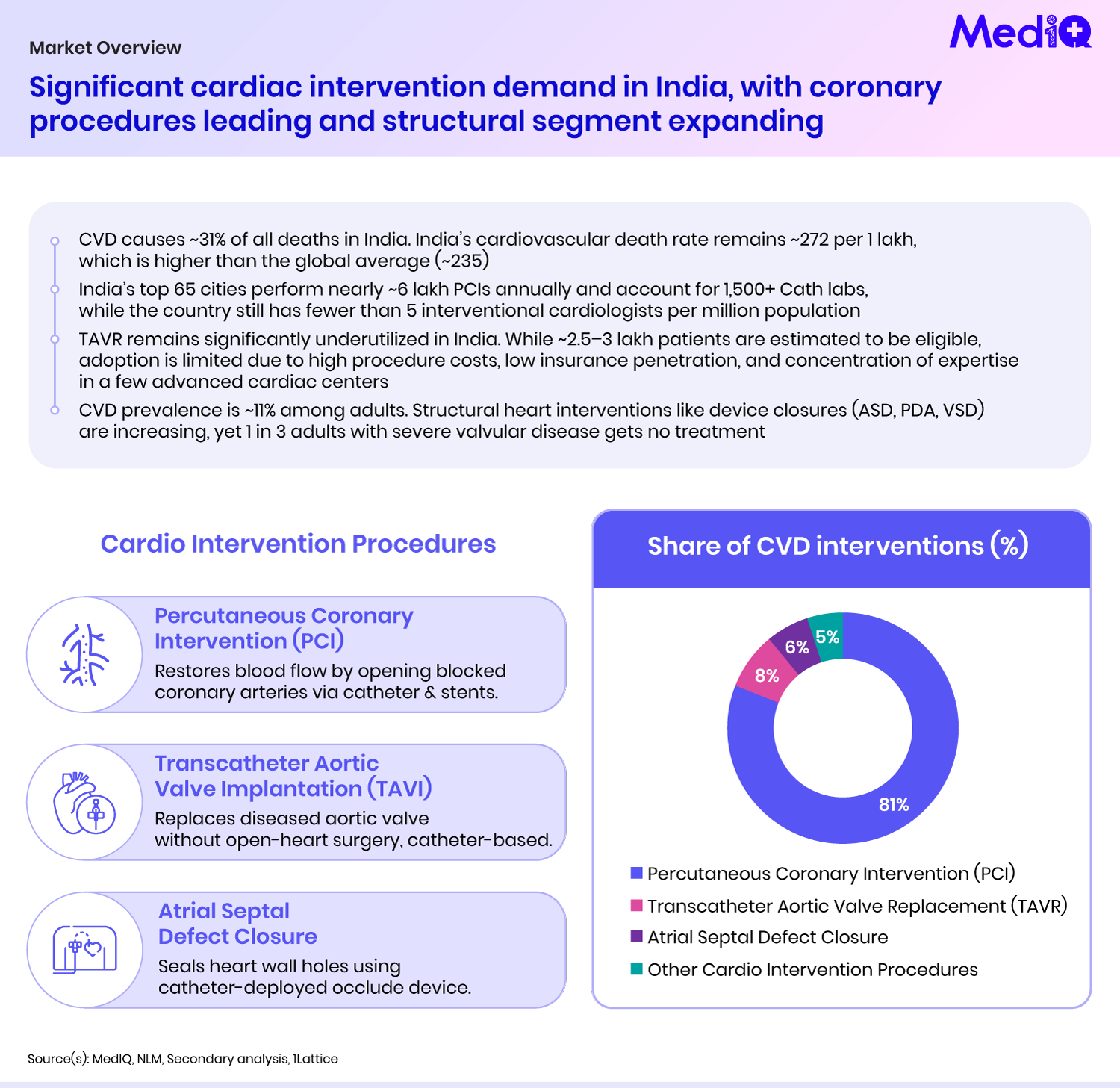

CVD accounts for ~31% of all deaths in India, with a cardiovascular death rate of ~272 per 1 lakh—higher than the global average. India’s top 65 cities perform nearly ~6 lakh percutaneous coronary interventions (PCI) annually, supported by 1,500+ cath labs, though access remains constrained with fewer than 5 interventional cardiologists per million population. PCI continues to dominate the intervention landscape, accounting for ~80%+ of procedures.

At the same time, structural heart interventions are gradually gaining traction. Transcatheter Aortic Valve Replacement (TAVR) remains underpenetrated despite an estimated 2.5–3 lakh eligible patients, primarily due to high costs, limited insurance coverage, and concentration of expertise in select centers. Additionally, interventions such as ASD, PDA, and VSD closures are increasing, although a significant proportion of patients with severe valvular disease still remain untreated. Overall, the Indian cardiac intervention space reflects strong demand fundamentals with substantial headroom for growth, particularly in structural and advanced therapies.

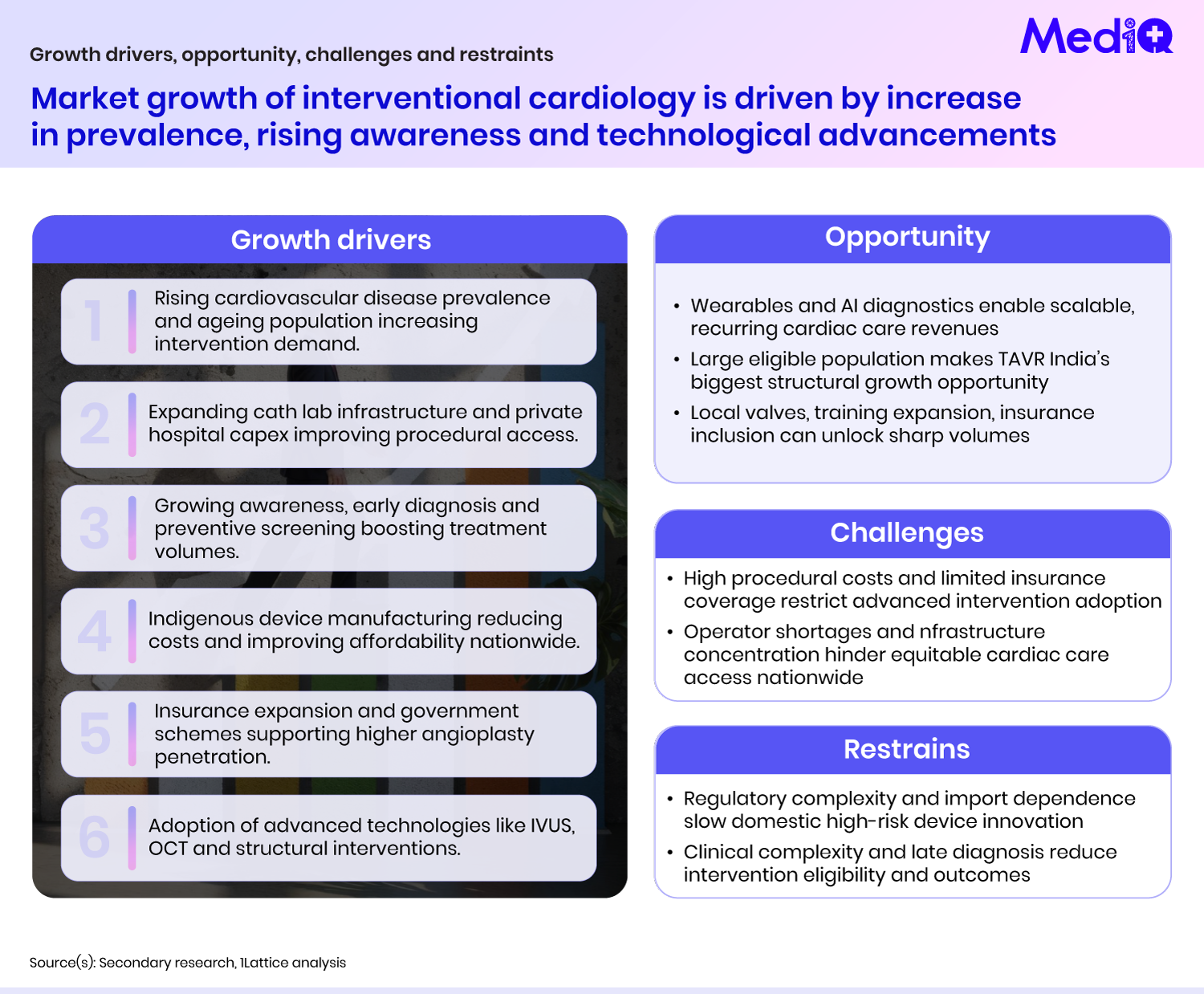

Interventional cardiology market growth in India is being driven by a rising burden of cardiovascular diseases, an ageing population, and increasing awareness leading to higher diagnosis and treatment rates. Expansion of cath lab infrastructure and private hospital investments is improving procedural access, while government schemes and insurance coverage are supporting higher angioplasty penetration. Additionally, the adoption of advanced technologies such as IVUS, OCT, and structural heart interventions is further accelerating market growth.

At the same time, the sector presents strong opportunities. Wearables and AI-enabled diagnostics are enabling scalable and recurring cardiac care models, while a large untreated patient pool makes structural interventions like TAVR a significant growth opportunity. Increased local manufacturing, training expansion, and broader insurance inclusion are expected to unlock higher procedure volumes.

However, key challenges persist. High procedural costs and limited insurance coverage continue to restrict the adoption of advanced interventions, while shortages of skilled operators and concentration of infrastructure in urban centers limit equitable access across the country.

Additionally, regulatory complexities and continued dependence on imports for high-end devices slow down domestic innovation. Clinical complexity and late-stage diagnosis further reduce intervention eligibility and impact overall patient outcomes, highlighting the need for systemic improvements in early detection and access.

Recent developments in India’s interventional cardiology space highlight strong momentum driven by both domestic and global investments, alongside increasing focus on innovation, research, and advanced patient care.

Indian MedTech player Polymed has expanded its cardiology portfolio through strategic acquisitions, strengthening its presence in cath lab consumables and devices. Similarly, Meril has attracted significant global investment, with Abu Dhabi’s ADIA investing ~$200 million, underscoring investor confidence in India’s fast-growing cardiac device market.

On the innovation front, partnerships such as Bayosthiti AI’s collaboration with Narayana Health to build a large-scale cardiac AI dataset are accelerating the adoption of data-driven diagnostics and personalized care. At the same time, consolidation activities like Translumina’s merger with Everlife are creating stronger, integrated cardiac device platforms in India.

Global players are also increasing their footprint. Companies like Foldax have introduced advanced heart valve technologies in India, while MicroPort has secured regulatory approval for its TAVR valve, expanding access to structural heart interventions.

Overall, these developments indicate a rapidly evolving ecosystem supported by capital inflows, strategic collaborations, regulatory progress, and technology innovation—positioning India as a key growth market for interventional cardiology.

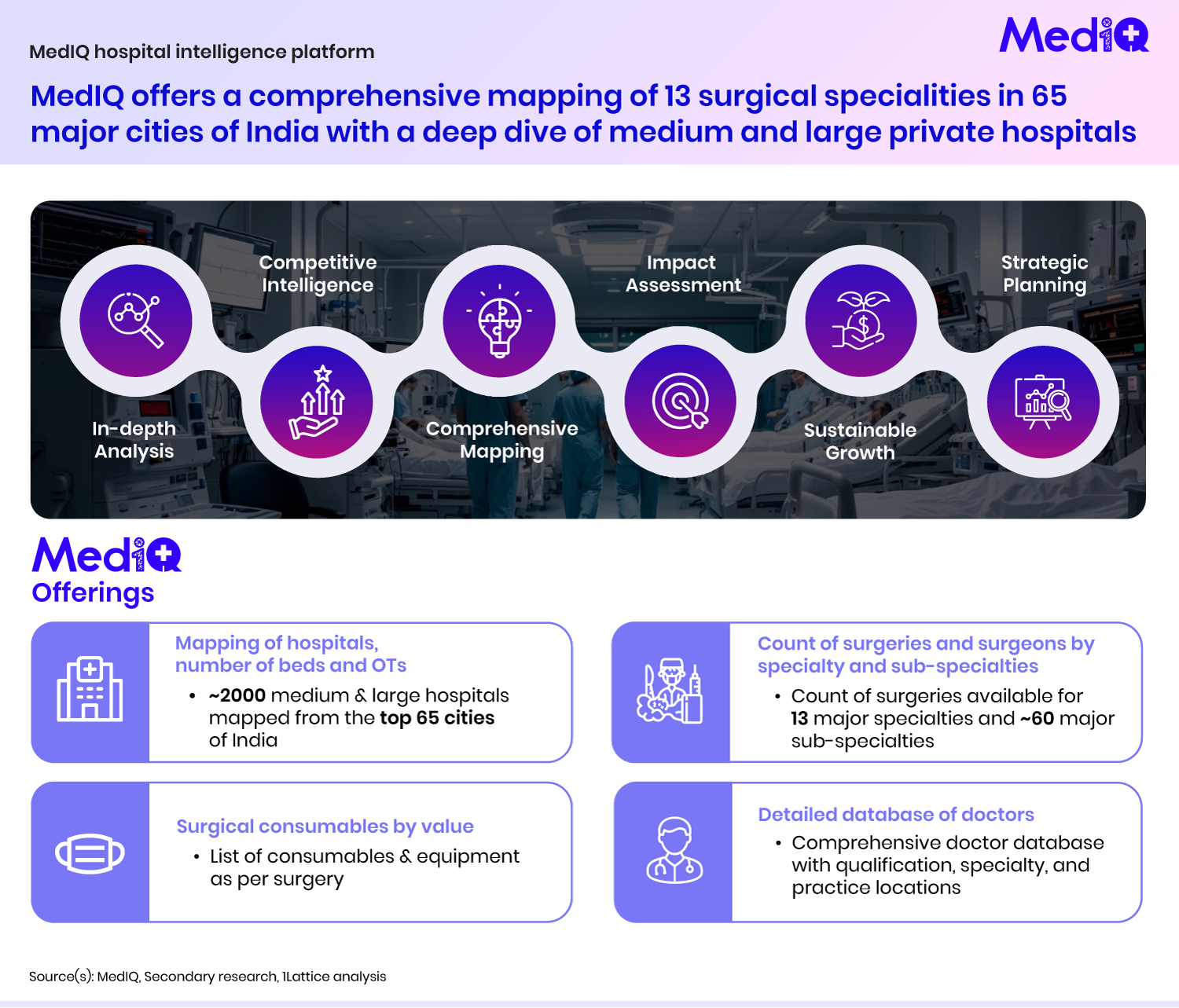

MedIQ by 1Lattice is a comprehensive hospital intelligence platform that enables MedTech leaders to take data-led decisions on procedure-driven demand and hospital readiness. It maps ~2,000 medium and large private hospitals across 65+ cities in India and delivers market sizing across 13 surgical specialties and ~60 sub-specialties, along with insights on surgical volumes, infrastructure, and utilization trends.

The platform provides in-depth analysis and competitive intelligence through comprehensive mapping of hospitals, including key parameters such as number of beds, operating theatres (OTs), and facility capabilities. It enables impact assessment by tracking procedure volumes and surgeon availability across specialties, while also supporting strategic planning through detailed insights into demand patterns and growth opportunities.

MedIQ offerings include a robust database of surgical procedures and surgeons across 13 major specialties, along with a detailed doctor-level dataset capturing qualifications, specialties, and practice locations. Additionally, it offers procedure-level mapping of surgical consumables and equipment, helping stakeholders understand value pools and product demand.

Overall, MedIQ serves as a one-stop solution for MedTech companies to drive sustainable growth through data-backed decision-making, market prioritization, and targeted commercial strategies across India’s hospital ecosystem.