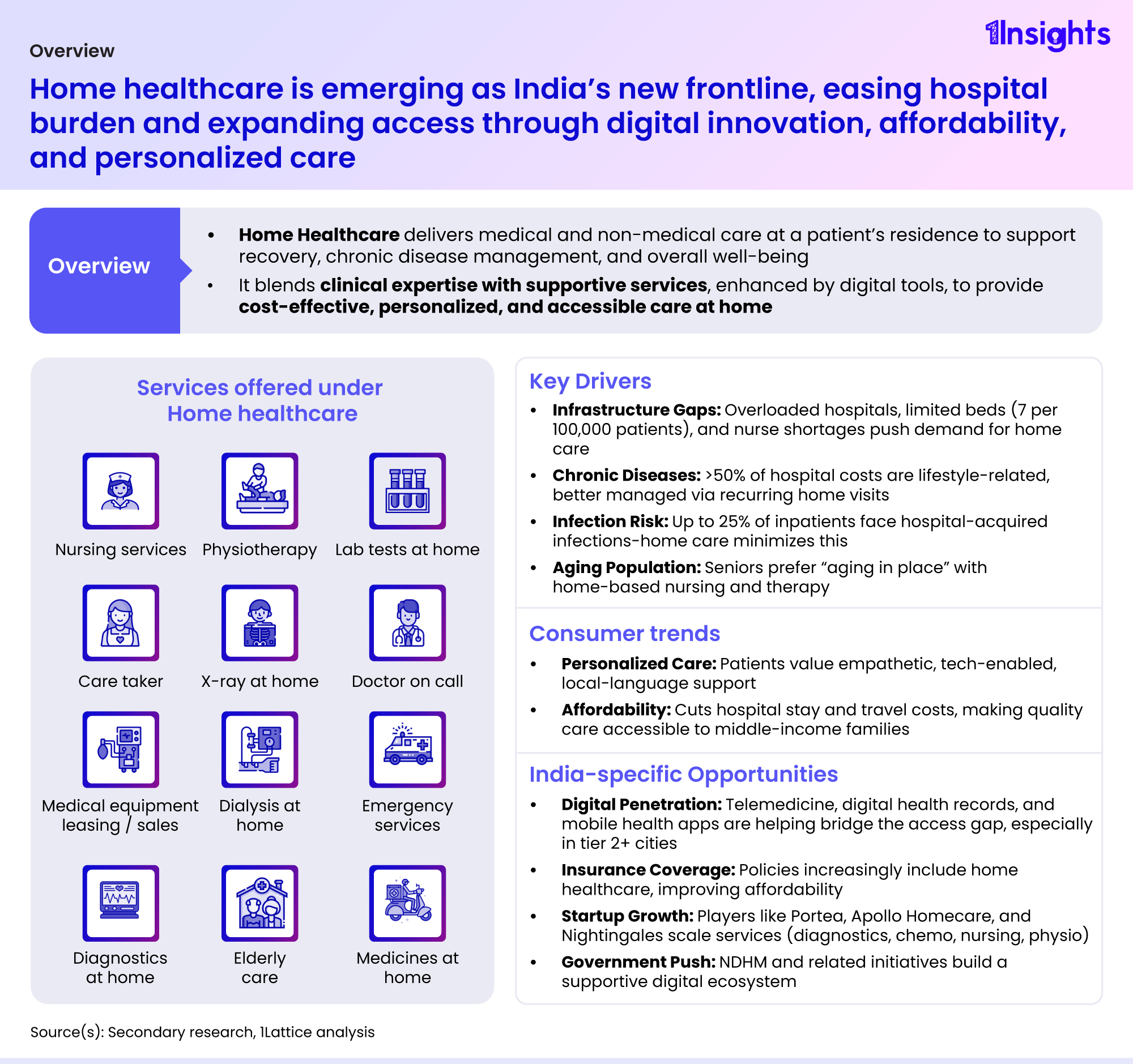

Blending clinical expertise with supportive non-medical services powered by digital innovations helps reduce the burden on hospitals while ensuring cost-effective and personalized care in the comfort of patients’ homes.

The scope of services has expanded significantly, covering nursing and caretaker support, doctor-on-call, physiotherapy, diagnostics and lab tests, dialysis, X-rays at home, medical equipment leasing, and elderly care. These offerings not only aid recovery but also strengthen chronic disease management, improving long-term health outcomes.

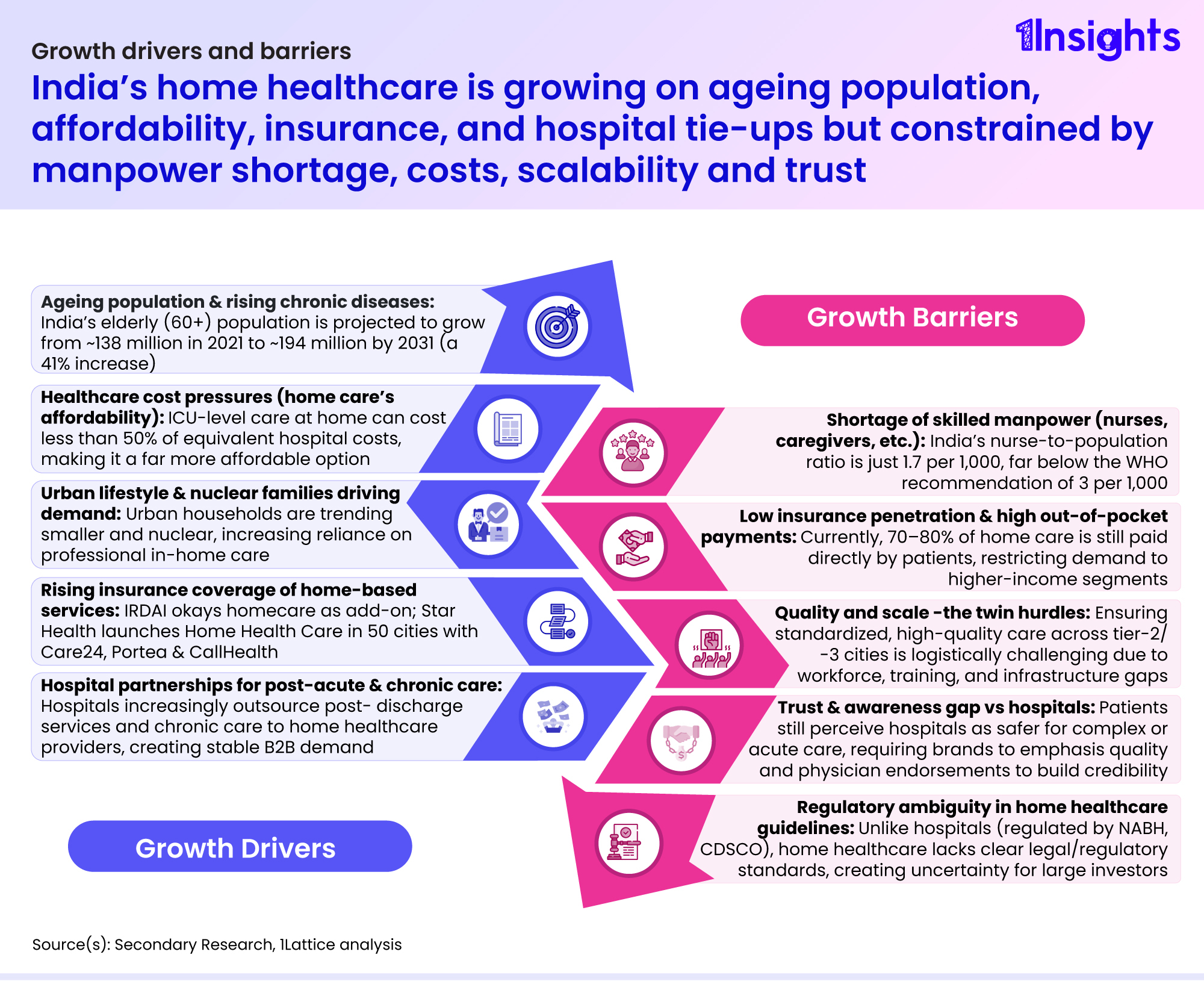

India’s need for home healthcare is pressing. With just seven hospital beds per 100,000 patients and a persistent shortage of nurses, hospitals are often overstretched. More than half of hospital costs today stem from lifestyle-related chronic disease conditions that can be better managed with recurring home visits. At the same time, up to a quarter of hospital inpatients face the risk of hospital-acquired infections, a challenge that home-based care significantly minimizes. Compounding these issues is India’s rapidly aging population, projected to rise by 41% between 2021 and 2031, who increasingly prefer “aging in place” with home-based nursing and therapy.

Consumer behaviour is also shifting. The rapid rise of telemedicine, digital health records, and mobile health apps is bridging access gaps, particularly in tier-2 and tier-3 cities. Insurance is beginning to play a supportive role, with the IRDAI approving home care as an add-on and insurers like Star Health partnering with Care24, Portea, and CallHealth to expand coverage. Startups such as Portea, Apollo Homecare, and Nightingales are scaling services, while government initiatives under the National Digital Health Mission (NDHM) are creating a strong digital backbone for growth

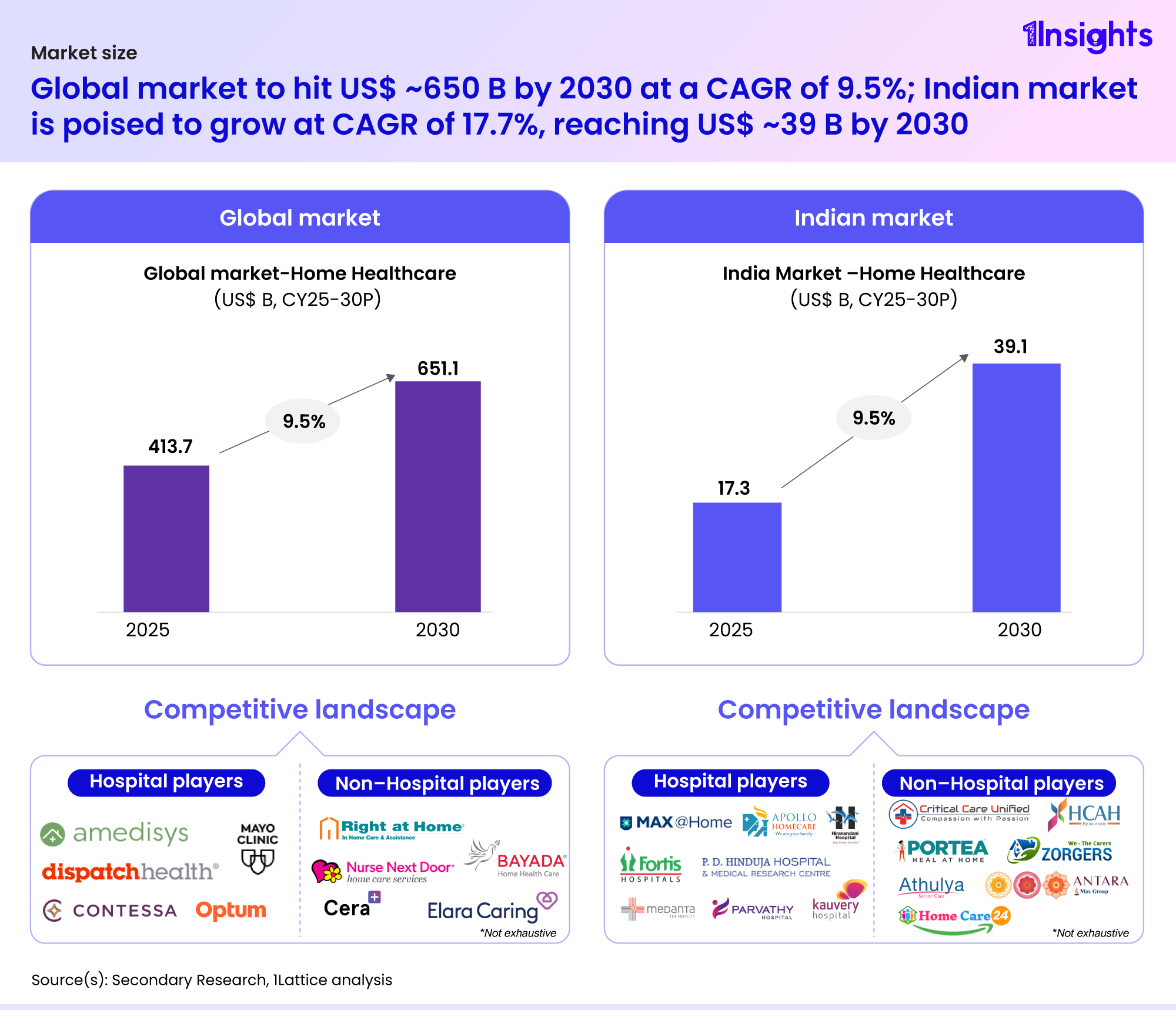

The market potential is significant. Globally, home healthcare is expected to reach nearly USD 650 billion by 2030, growing at a CAGR of 9.5%. India, however, is poised to grow at nearly double that pace, 17.7% annually, to reach USD 39 billion by 2030. This growth is driven by an aging population, affordability advantages (ICU-level care at home can cost less than half of hospital equivalents), rising insurance coverage, and evolving family structures that increase reliance on professional in-home care

The market potential is significant. Globally, home healthcare is expected to reach nearly USD 650 billion by 2030, growing at a CAGR of 9.5%. India, however, is poised to grow at nearly double that pace, 17.7% annually, to reach USD 39 billion by 2030. This growth is driven by an aging population, affordability advantages (ICU-level care at home can cost less than half of hospital equivalents), rising insurance coverage, and evolving family structures that increase reliance on professional in-home care

Challenges, however, remain. India’s nurse-to-population ratio is just 1.7 per 1,000, far below the WHO’s recommended 3. Out-of-pocket payments continue to dominate, with 70–80% of home care expenses borne directly by patients. Unlike hospitals regulated by NABH or CDSCO, home healthcare lacks clear regulatory guidelines, creating uncertainty for large-scale investments. Moreover, scaling standardized, high-quality care across smaller cities remains difficult, and trust gaps persist as many patients continue to view hospitals as safer for acute or complex conditions.

Despite these hurdles, the investment momentum is strong. In February 2025, a $37.5 million Series B funding round led by Accel (with IFC, Qualcomm Ventures, and Ventureast) highlighted rising VC and PE interest in scaling in-home clinical services. Japan’s Human Life Management (HLM) acquired an Indian home healthcare player in 2022, reflecting cross-border expansion opportunities. Strategic buyouts in 2022–23, including by Medwell SA, show active consolidation, while PB Healthcare raised $218 million in one of India’s largest seed rounds to build an integrated, value-based care platform with potential home-centric solutions.