In the aftermath of the COVID-19 pandemic, there has been a noteworthy surge in Non-Banking Financial Companies (NBFCs) contribution to the education loans segment. This surge underlines the evolving landscape of educational financing, with NBFCs poised to play a pivotal role in shaping the accessibility and availability of funding for aspiring learners.

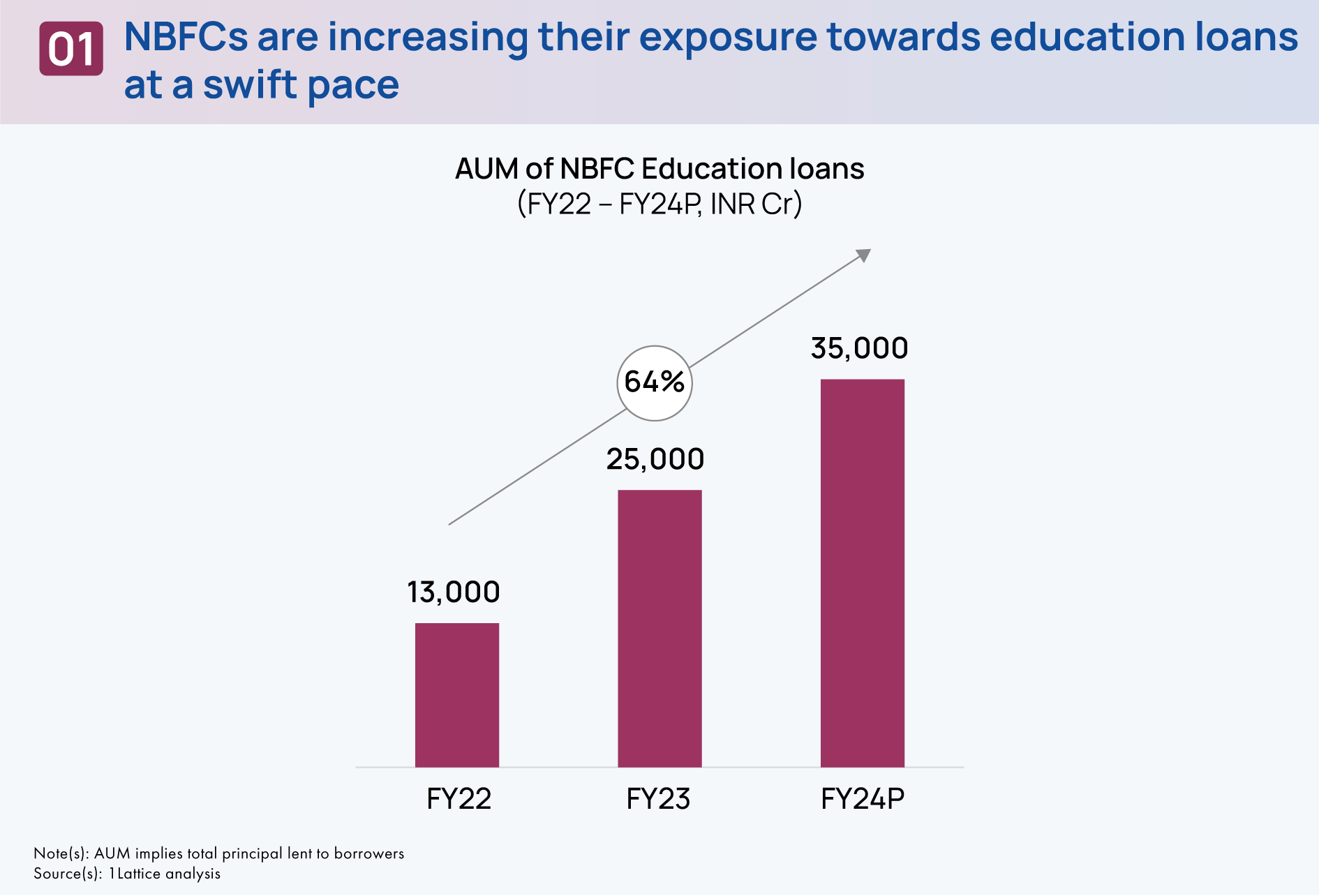

The assets under management (AUM) for educational loans disbursed

by NBFCs are expected to grow at 40% Y-o-Y from INR 25,000Cr in FY23 to INR

35,000Cr in FY24. This growth can be primarily attributed to the distinctive

and specialized business models of NBFCs which tend to give them an edge over

banks. These models are characterized by several key elements that contribute

to their success which are as follows:

- ·

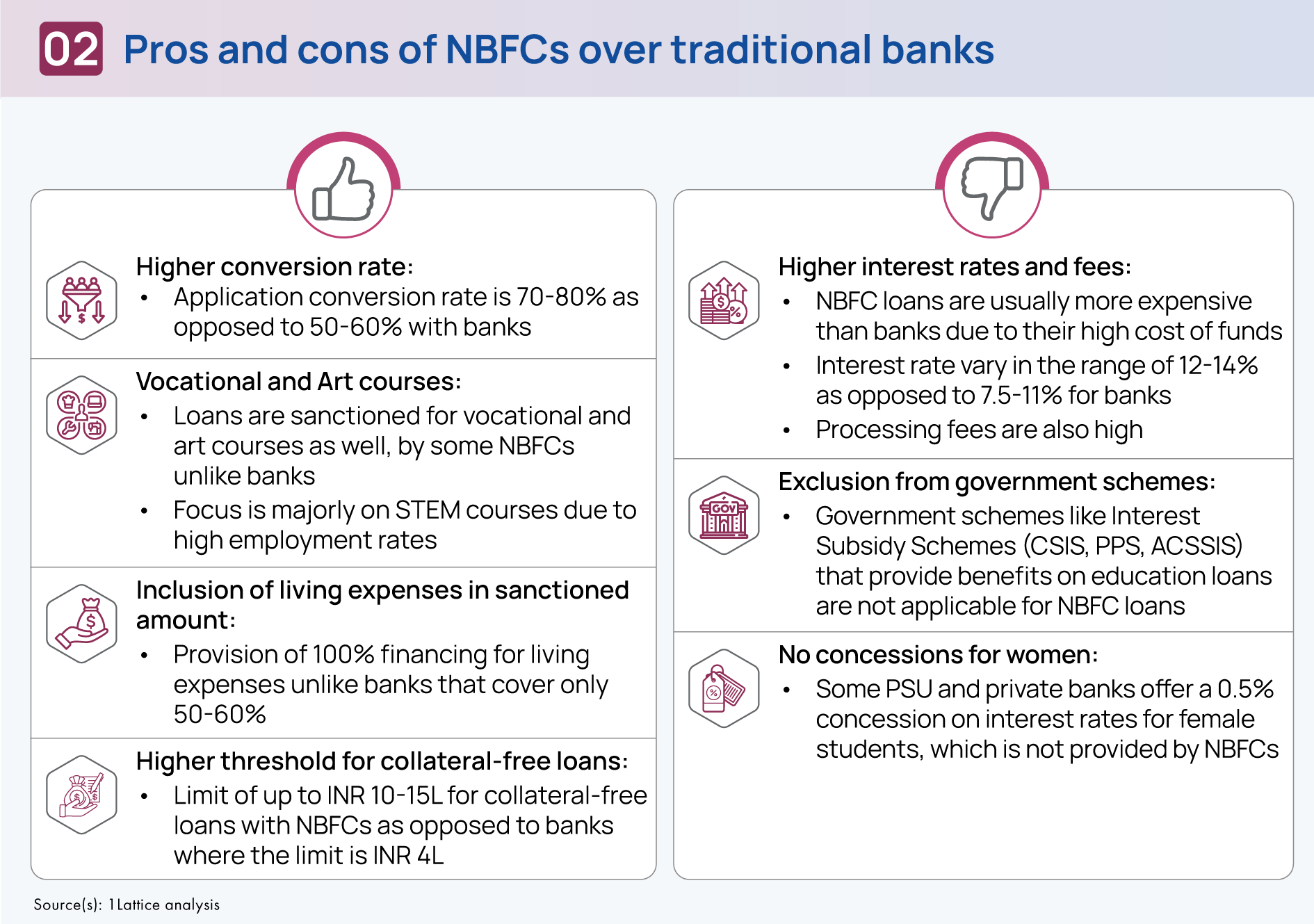

Allowing the applicant’s distant relatives to be

co-borrowers unlike banks which permit only parents to become co-applicants

- ·

Speedy disbursal of loans due to comparatively

simplified processes as compared to banks

- · Even though there is a strategic focus on Science, Technology, Engineering, and Mathematics (STEM) courses, renowned for their high employability rates, NBFCs also sanction loans for vocational and art courses

- · Flexible repayment terms like longer moratorium period, increase in no. of EMIs, etc.

NBFCs present distinct advantages, such as impressive conversion rates due to focused strategies, and the willingness to fund non-STEM courses among others. However, challenges like higher costs and the absence of interest subsidy schemes like Central Scheme of Interest Subsidy (CSIS), Padho Pardesh Scheme of Interest Subsidy (PPS), Dr. Ambedkar Central Sector Scheme of Interest Subsidy (ACSSIS) that are typically available through traditional bank loans act as headwinds.

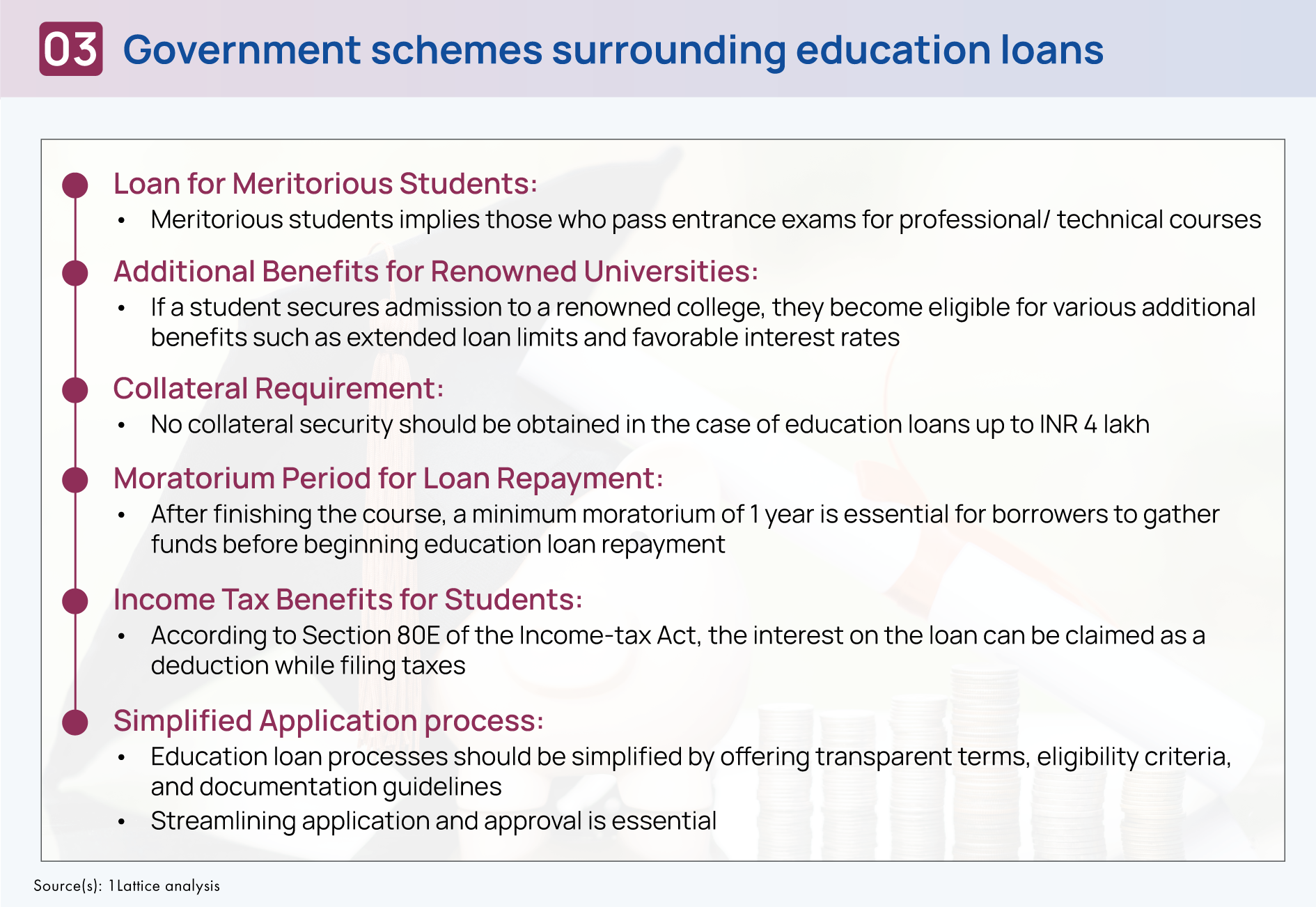

The government has introduced certain schemes to make

education financing simpler and easier for both borrowers and lenders. By

giving these instructions, the government wants to motivate lenders to offer

education loans without making things too hard and to make sure more deserving

students can avail of them.

This shift presents advantageous opportunities for NBFCs

such as HDFC Credila, Avanse, Auxilo, InCred, and others that are already

active in the education loan sector. It also opens up new chances for NBFCs

that specialize in education loans. These NBFCs can capitalize on the changing

preferences of students and expand their services to cater to the increasing

demand for education loans in these new study destinations.