India’s population is steadily ageing, and with it, the importance of long-term financial planning has come to the forefront. As life expectancy increases and traditional support systems like joint families evolve, there is growing awareness around building a secure post-retirement life.

Public and private initiatives are converging to build a more inclusive and accessible retirement ecosystem, encouraging individuals across income segments to invest actively in their future actively.

India’s retirement product landscape has grown substantially over the past decade, with two key pillars, the National Pension System (NPS) and Atal Pension Yojana (APY), driving this momentum.

As of June 30, 2025, APY has surpassed 6.6Cr subscribers, managing assets worth INR 47,643Cr, with an average annual return of 9.11% since inception.

NPS has also witnessed steady adoption, with over 2.02Cr subscribers and a growing corpus exceeding INR 14.91L Cr (Jun 25). The equity tier of NPS has delivered a CAGR of 14.2% since inception.

The steady rise in retirement product subscriptions in India is a result of multiple converging factors, both structural and policy-driven. India’s rising retirement product subscriptions are driven by a combination of demographic changes, supportive government policies, growing financial awareness, digital access, and appealing returns. Programs like NPS and APY have expanded reach, especially among informal workers, while improved onboarding processes and tax benefits continue to make pension planning more accessible and attractive to a broader population. As adoption continues to accelerate, the benefits are increasingly visible for institutions, individuals, and the broader economy.

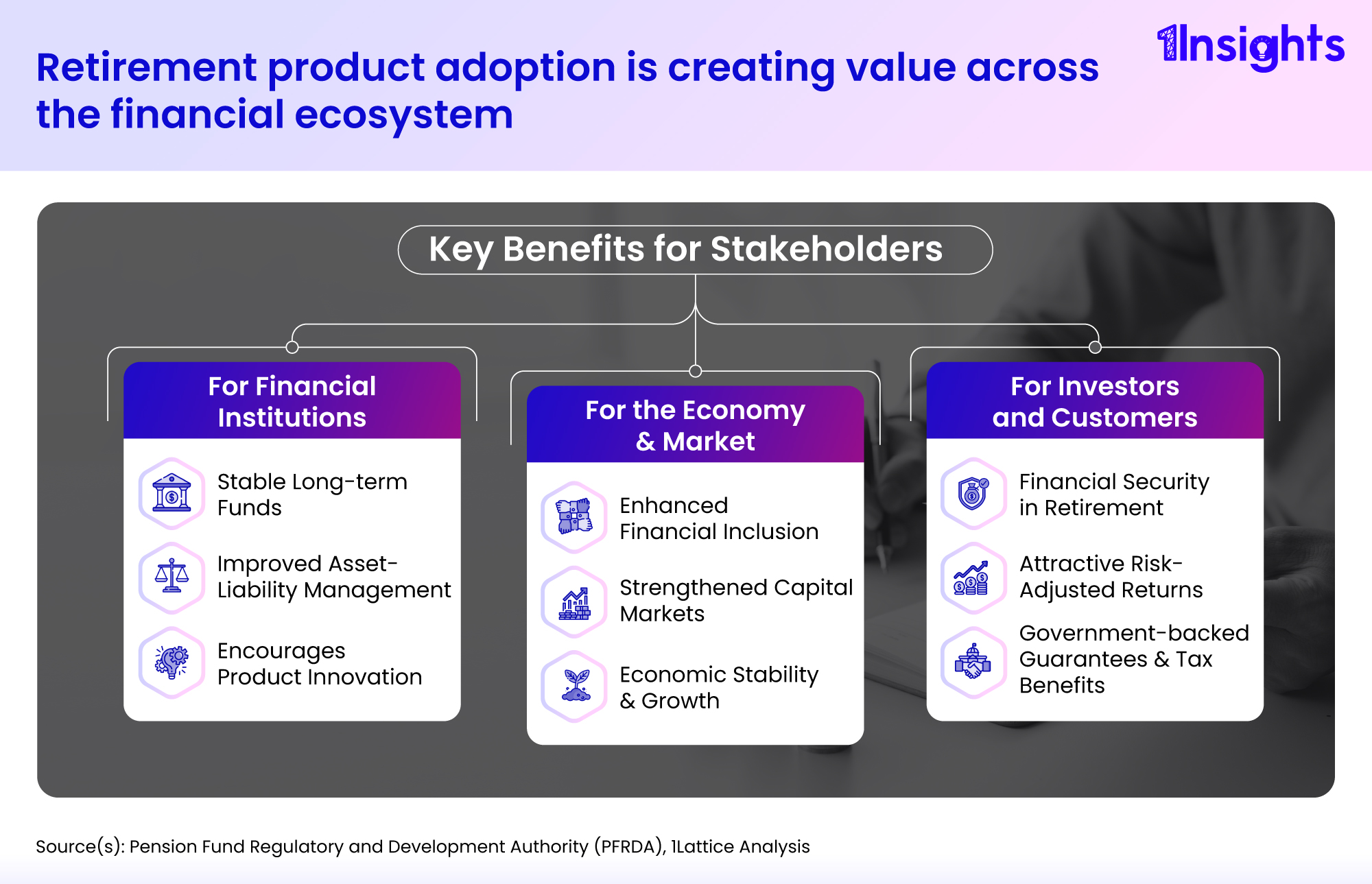

The expanding adoption of retirement products offers significant advantages across the financial ecosystem. For financial institutions, increased subscriptions mean a steady inflow of long-term funds, improving asset-liability management and reducing reliance on short-term borrowing. This stability fosters innovation, competition, and better service quality for consumers.

For investors, these products promote disciplined savings, ensuring greater post-retirement security. Schemes like the National Pension System (NPS) and Atal Pension Yojana (APY) offer attractive risk-adjusted returns, government-backed guarantees, and tax benefits, making retirement planning more accessible and rewarding. Private sector participation, aided by technology and regulatory support, is expanding financial inclusion, strengthening capital markets, and boosting economic stability

The steady rise in subscriptions and corpus reflects growing awareness of retirement planning in India. With continued regulatory backing, digital expansion, and targeted outreach, these products can become a cornerstone of inclusive financial well-being. Addressing challenges around trust, income volatility, and access will be vital for deeper penetration and long-term success.