Overview

In recent years, artificial intelligence (AI) & data science have slowly become an integral part of business decision-making. It has helped new-age businesses become more customer-centric by better forecasting demand, inventory management, and targeting customers effectively through personalized recommendations. Moving towards immersion of AI in the BFSI sector, logistic regression-based credit scoring, automated claim processing, and robo-advisors/chatbots are some of the areas where it has already established its presence.

In today’s newsletter, we look at how AI & data science can have an impact on the lending landscape in India.

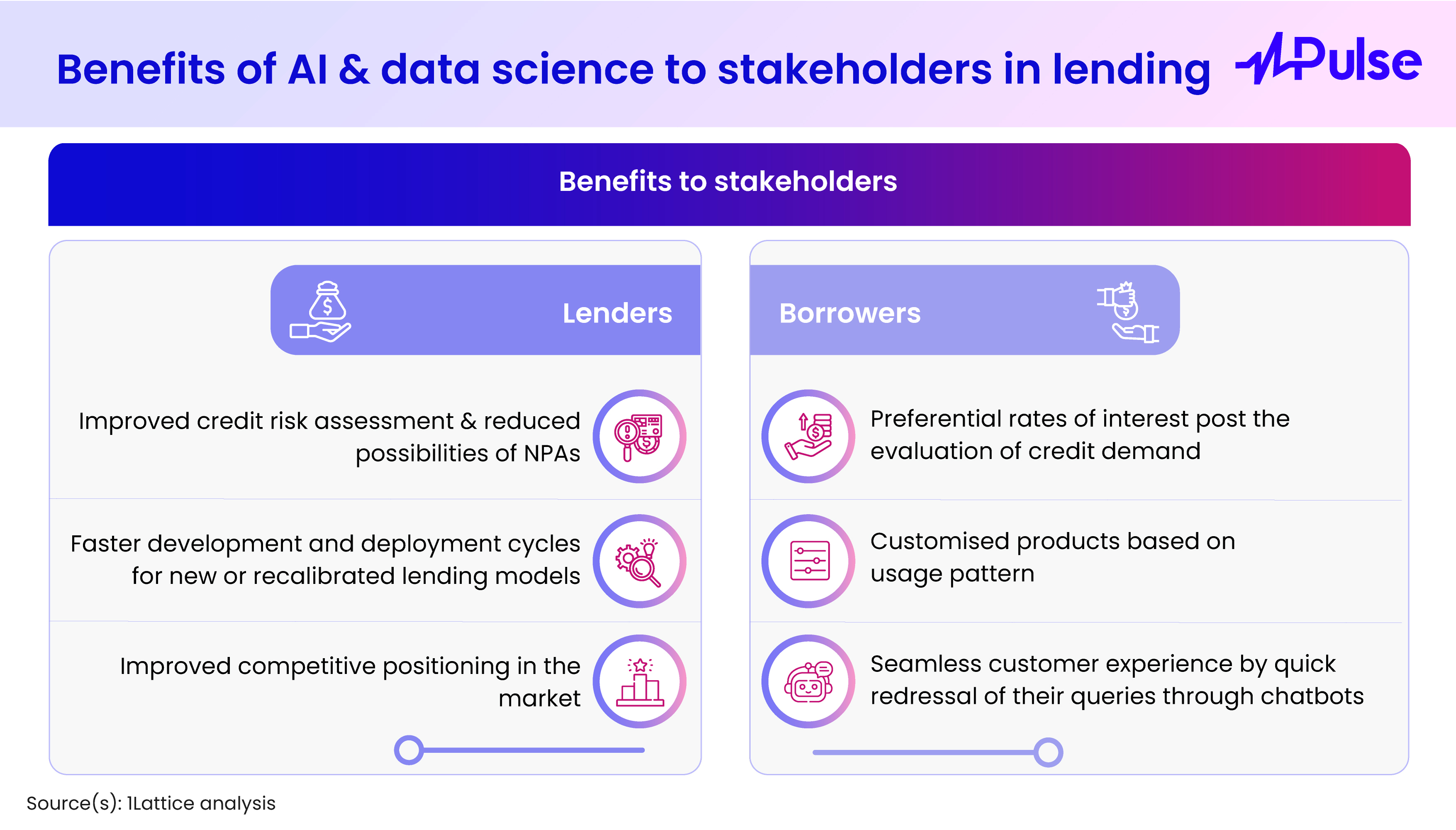

India’s digital lending market was estimated to be ~ US$ 70B in 2023 and is expected to reach US$ 515B by 2030, growing at a CAGR of 33%. Integration of AI in lending processes enables lenders to make more informed decisions, streamline operations, improve risk management, and enhance the customer experience.

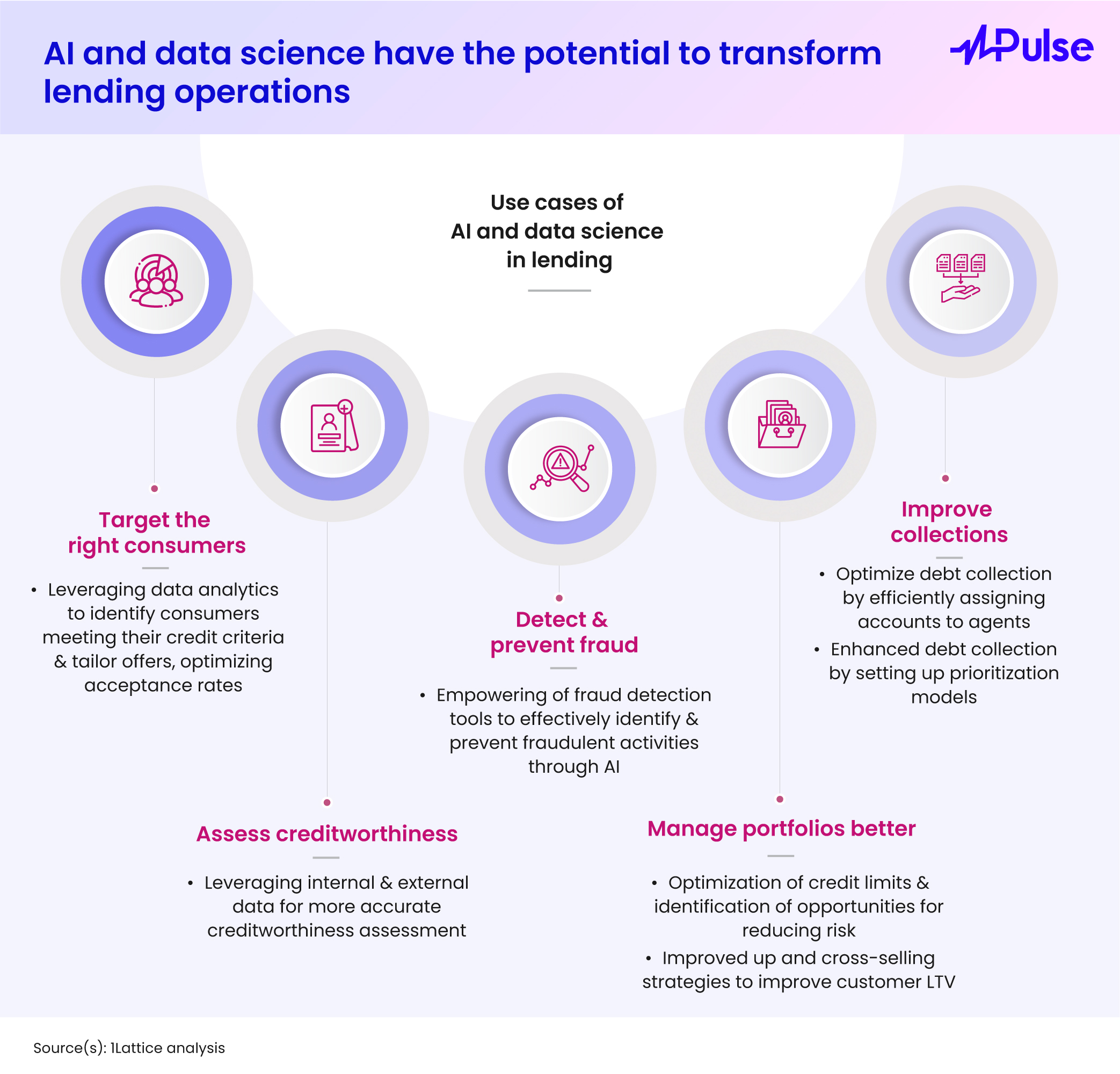

AI-driven tools are being implemented throughout the customer lifecycle for a variety of reasons.

- Lenders can sift through extensive datasets to identify consumer cohorts thus aligning their credit criteria better. It helps provide these consumers with more tailored and personalized offers. This entails providing small loans or microfinance to diverse segments of the population, especially those who may not fit the conventional mold of creditworthiness.

- AI fraud detection is a technology-based approach that employs machine learning to identify fraudulent activities within large datasets. It involves training algorithms to recognize patterns and anomalies that signal possible fraud. These models continuously attune themselves based on new data improving their predictive accuracy and helping maintain transaction integrity and security.

- Machine learning-driven models can integrate various internal and external data points to accurately assess creditworthiness. A broader range of data points like bank account transaction history, utility bill payment history, alternative data sources (with permission) like cash flow from freelance work, and public information can be considered by the models to assess the credit score of the applicant.

- Enhanced evaluations can streamline the flow of applications into automated approval and denial processes, minimizing the need for manual review. Lenders develop models trained on historical data of approved and rejected loans which analyze factors like applicant's credit score, income and employment history, debt-to-income ratio, loan purpose, etc.

- By leveraging comprehensive insights into their customer base, lenders can make informed decisions regarding initial credit limits and identify opportunities to reach out to underserved customers. Additionally, AI-driven models aid in identifying opportune moments to up and cross-sell products and determine the most effective outreach strategies.

- Models can be developed to streamline debt collection procedures, including account allocation, prioritization, and consumer contact strategies. For example, AI and ML algorithms work seamlessly to recover delinquent customers by looking at customers’ technographic, geographic, and psychographic touchpoints.

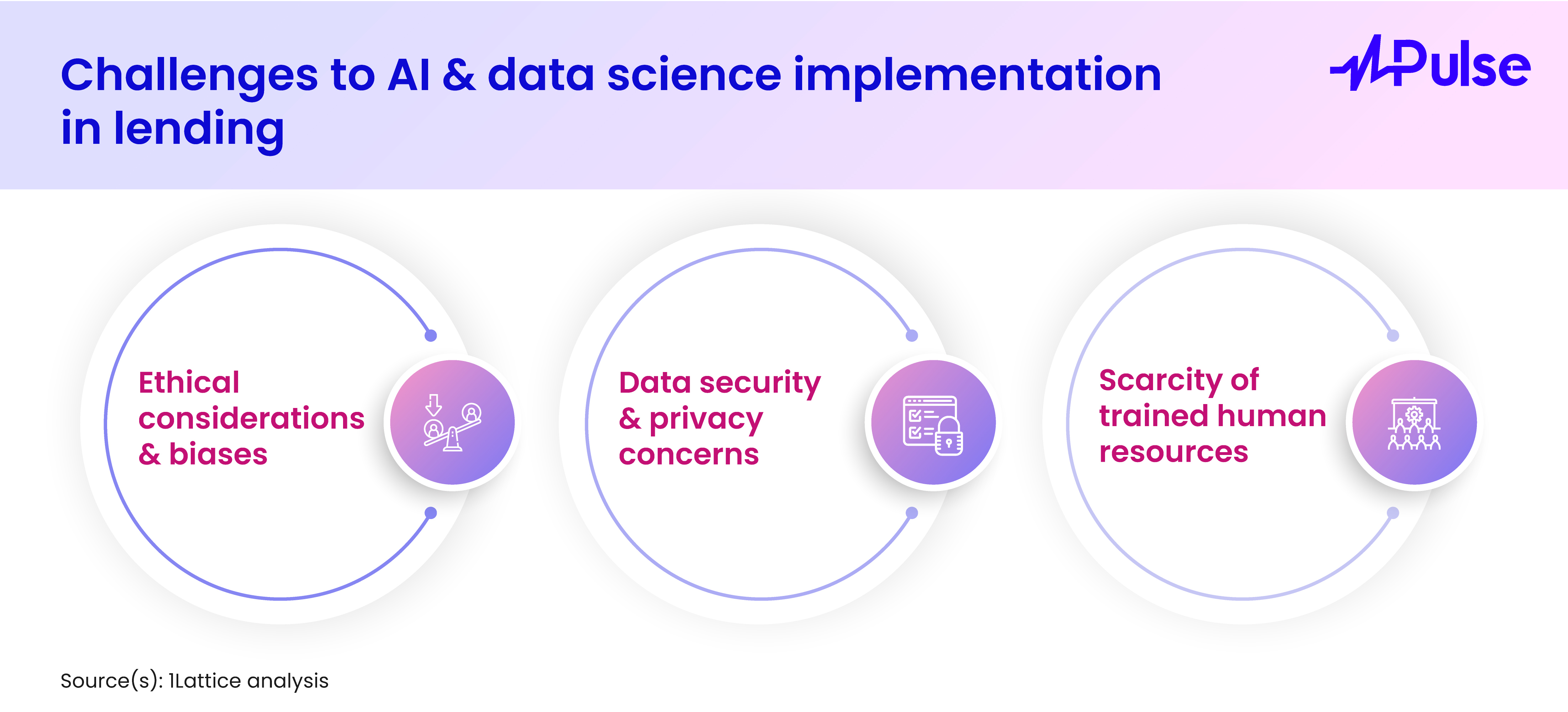

While there are multiple uses of AI in lending, its widespread adoption still faces some concerns: